The American Compute Corridor Through Russia. The Alternative to the Gulf?

The Ukraine peace plan named AI, data centers, and Arctic rare earths as pillars of long-term US-Russia economic cooperation. Putin’s 9 May overture puts the plan back on the table.

On 9 May, speaking after Victory Day, Vladimir Putin said the war in Ukraine “is coming to an end,” named former German chancellor Gerhard Schröder as his preferred negotiator for a Russia-Europe security track, and indicated readiness to meet Volodymyr Zelensky in Moscow or a third country to sign a final agreement. EU foreign ministers rejected the Schröder proposal three days later. The 28-point American peace framework that leaked in late November 2025, dormant for most of the spring while the Iran conflict absorbed Washington’s attention, is back on the table.

The coverage of that framework has centred on the $100 billion in frozen Russian assets, the Ukrainian army cap, and the territorial clauses around Donetsk. Four other clauses describe something different. Provision 12 sets up a Ukraine Development Fund to invest in “fast-growing industries, including technology, data centers, and artificial intelligence.” Provision 13 commits the United States to a “long-term economic cooperation agreement” with Russia in “energy, natural resources, infrastructure, artificial intelligence, data centers, rare earth metal extraction projects in the Arctic, and other mutually beneficial corporate opportunities.” Provision 14 funds a US-Russia investment vehicle from what remains of the frozen Russian assets after Ukrainian reconstruction. Provision 19 places the Zaporizhzhia nuclear plant, 5.7 gigawatts of capacity, under IAEA supervision with electricity shared 50:50 between Ukraine and Russia.

These four clauses describe three different compute propositions. They are worth distinguishing because Russia, Ukraine, and the Gulf each play a fundamentally different role in whatever post-war infrastructure stack actually gets built.

Ukraine, as I argued in an earlier piece, is assembling the inputs for European sovereign compute: nuclear baseload through Energoatom and the planned Westinghouse AP1000s, distributed generation that DTEK doubled to 5,144 installations in 2025, 200 MW / 400 MWh of grid-forming batteries dispersed across six sites, and 31 bcm of underground gas storage (the largest in Europe, third globally). On top of that hardware, Ukraine is building a credential layer through the Diia.Engine state platform and the Guarantees of Origin registry that will integrate into the EU Association of Issuing Bodies by 2027. That layer matters because it makes Ukrainian clean electricity exportable as auditable compute under European green-accounting rules. Ukraine is not a candidate for an American hyperscale corridor. It is being assembled for the European one.

Russia is the opposite proposition. It will not build frontier models. It does not have the labs, the talent base, or the capital. What it does have is the asset profile that any large data center developer recognises immediately: roughly 20 percent of the world’s natural gas reserves, the largest in the world; surplus grid capacity built for a Soviet-era industrial demand that no longer exists; Arctic minerals that bypass Chinese chokeholds on gallium, germanium, and heavy rare earth magnets; and, in the peace plan, joint operation of the largest nuclear plant in Europe. Where Ukraine is building a credentialed, green-accounting stack legible to European regulators, Russia is offering raw, un-vetted, brute-force scale.

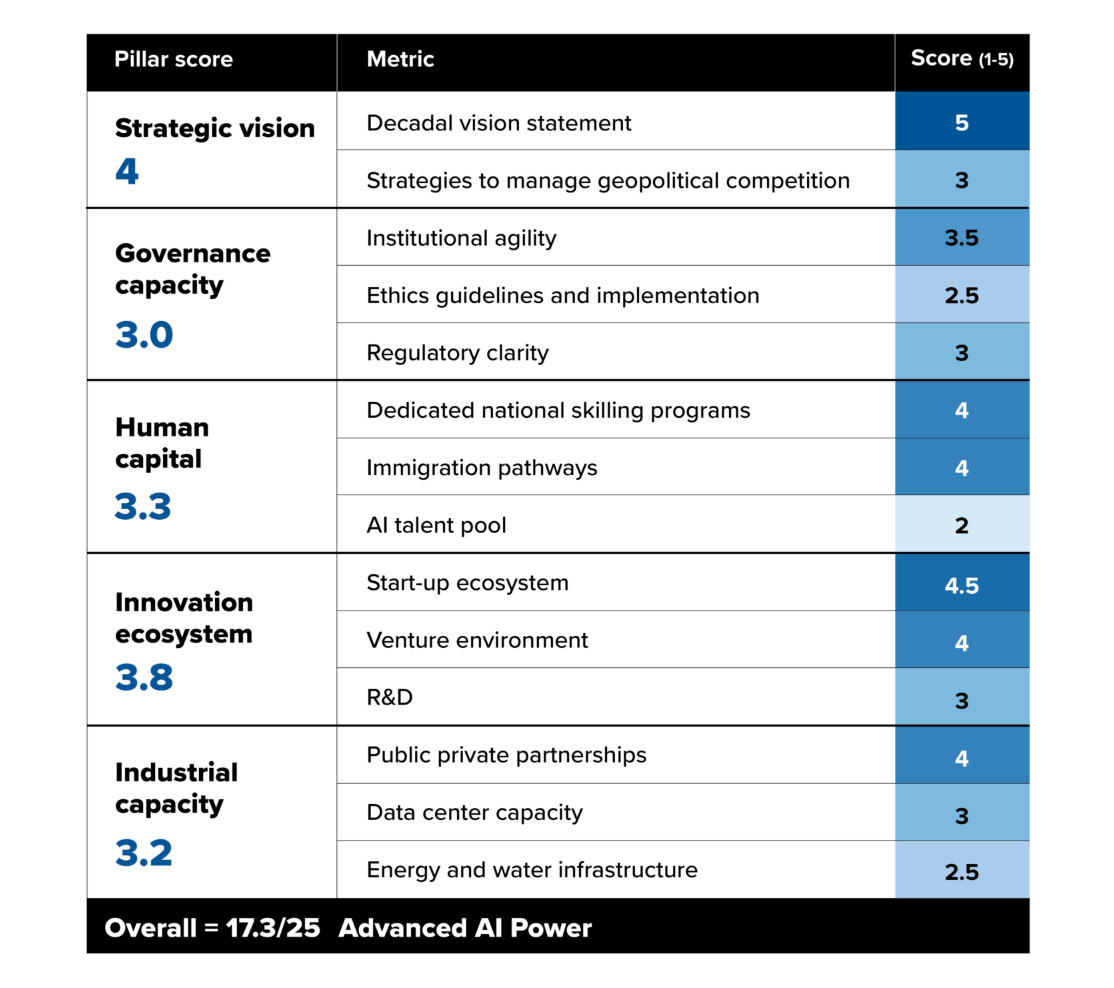

The Gulf model is in execution and is the benchmark every other proposition is now measured against. Stargate UAE, a 5-gigawatt campus in Abu Dhabi at more than $30 billion, opens its first 200 megawatts in Q3 2026. Saudi Arabia’s HUMAIN, chaired by the Crown Prince, targets 1.9 gigawatts of data center capacity by 2030 and 6.6 gigawatts by 2034, with a 600,000-GPU agreement signed with Nvidia. The Atlantic Council GeoTech Center’s May 2026 issue brief by Trisha Ray and Raul Brens Jr. assesses the UAE as an “advanced AI power” at 17.5 out of 25, and recommends that the UAE itself co-invest in distributed compute capacity “across geographically dispersed locations outside the immediate region.”

The UAE has begun to operationalise that exact logic through G42’s Digital Embassies framework, launched at Davos in January 2026: a government-to-government legal construct that lets sovereign workloads run on UAE infrastructure while jurisdiction and control remain with the partner state. Sovereignty becomes portable. The infrastructure does not need to sit inside the customer’s borders.

Read against the Gulf, the Russian proposition in the peace plan offers structurally similar advantages: cheap energy, abundant minerals, sovereign-scale capital absorption through the investment vehicle in Provision 14, geographic distance from American grid constraints. The Gulf has executed. The Russian version is on paper.

The structural difference between the two corridors is the counterparty record and the American export control law. Under the Bureau of Industry and Security regime tightened repeatedly through 2024 and 2025 and codified again in the January 2026 final rule, frontier AI chips (the H100, B200, GB200 class) cannot be lawfully sited in Russia, which is a Tier 3 destination under the AI Diffusion Rule. Even a comprehensive peace settlement does not automatically reverse those controls; the BIS framework tracks not only where the rack sits but the nationality and headquartering of the end user, and applies worldwide licensing requirements to any firm headquartered in an arms-embargoed destination. The Russian compute corridor as written in Provision 13 cannot function as a standard hyperscale availability zone. To work at all, it would need a G42-type Greenshield-equivalent enclosure: physically air-gapped, US-managed, US-jurisdictional infrastructure where Russia supplies energy, security, and minerals, and nothing else. Washington may want the gas, but it cannot (under current law) trust the host with the chips.

A real-options reading of Provisions 13 and 14 is that the United States is not committing to build through Russia. It is reserving the right to. The clauses cost nothing to include and created two strategic effects at once. They gave Russia an economic reason to accept the political terms of the plan, because the corridor only opens if the war ends and only opens to the extent sanctions and BIS controls are unwound. And they put a floor price under the Gulf. By sketching a theoretical second offshore corridor in a treaty draft, Washington signals to Abu Dhabi and Riyadh that their monopoly on sovereign-scale, fast-to-connect power is not mathematically permanent. The clauses introduce a benchmark even if no hyperscaler ever signs a letter of intent.

Whether any of this materialises depends on what Europe does next. Putin’s 9 May overture was not primarily directed at Washington. It was directed at Berlin, and through Berlin at the European capital flows that Russia actually needs. There is a logic for Europe to seek accommodation with a weakened Russia: access to natural resources in exchange for European capital and a settlement that stabilises the eastern flank. The E3 counter-proposal of November 2025 already stripped Provisions 13 and 14 out of the plan, replacing the US-Russia investment vehicle with a multilateral reparations framework. Brussels accelerated a separate €140 billion frozen-assets scheme that Friedrich Merz called the negotiating consensus across European capitals. The fight inside the peace plan is no longer between Washington and Moscow, but between Washington and Brussels over who reintegrates Russia and on what terms.

If Brussels wins that contest, Russia becomes an energy appendix to Europe’s green transition: gas and Arctic minerals flowing into European industrial systems, with the American compute corridor staying on paper.

If Washington wins, Russia is integrated into a transactional, bilateral compute-monetisation engine, and the Gulf gains a benchmark competitor that will tighten pricing on the next round of Stargate-scale commitments. Either outcome shifts where the world’s compute gets built and which jurisdiction the data lives under.

Infrastructure investors have priced the offshore American map as if the Gulf were the only option. A second corridor is being written into a treaty draft this quarter. Ukraine is building the European one in parallel, under fire, for entirely separate reasons. Statecraft is compute. The peace plan is statecraft. Provisions 12, 13, 14, and 19 are where the three meet.

SOURCES

28-point plan text and Provisions 12, 13, 14, 19: Axios (20 Nov 2025), Al Jazeera (21 Nov 2025), ABC News (21 Nov 2025), The Hill, Newsweek (21 Nov 2025), CSIS The Unfinished Plan for Peace in Ukraine (9 Feb 2026), Belfer Center A Flawed Path to Peace (10 Dec 2025), Ukrainska Pravda full text release (23 Nov 2025).

Putin Victory Day 9-10 May 2026, Schröder proposal, Zelensky meeting offer: Al Jazeera (11 May 2026), TASS (9 May 2026), Milli Chronicle on EU foreign ministers’ rejection (12 May 2026).

Atlantic Council GeoTech Center, The new playbook for AI leadership: The case of the United Arab Emirates, Trisha Ray, Ryan Pan, Raul Brens Jr. (7 May 2026).

G42 Digital Embassies and Greenshield framework: G42 / Core42 launch announcement (Davos, January 2026).

E3 19-point counter-proposal: Reuters via Kyiv Post (24 Nov 2025), Ukrainska Pravda.

Merz on the EU consensus on frozen assets: ARD interview (24 Nov 2025), Anadolu Agency (5 Dec 2025).

Zaporizhzhia 5.7 GW: France 24 (29 Dec 2025), Newsweek (31 Dec 2025), Kyiv Independent (24 Dec 2025).

Russia natural gas reserves, Arctic LNG 2 status: Oxford Institute for Energy Studies (Oct 2024), Real Instituto Elcano (Jun 2024), IEA Global LNG Capacity Tracker (17 Mar 2026), Moscow Times via Bloomberg (1 Oct 2025).

Ukraine compute inputs: Sovereign Compute, Ukraine Is Assembling the Inputs for European Sovereign Compute (28 Apr 2026), and underlying sources cited there.

Stargate UAE and HUMAIN: The National (26 Jan 2026), G42 press release (May 2025), Middle East Institute From Crude to Compute (6 Feb 2026).

BIS export controls on advanced AI chips: Federal Register final rule 2026-00789 (15 Jan 2026), Mayer Brown briefing (22 Jan 2026), Morgan Lewis (16 Jan 2026), Introl AI export controls global tracker (Jan 2026), SemiAnalysis on AI Diffusion Rule tiering.

A NOTE ON INDEPENDENCE

All opinions shared in this newsletter are my own and do not reflect the views of dmg events, ADIPEC, or any affiliated organizations. This is personal analysis, not institutional positioning.