Ukraine Is Assembling the Inputs for European Sovereign Compute

Wartime decentralisation has produced exactly the topology European hyperscalers now need: clean baseload, distributed firming, and a credential layer auditable to EU green-accounting standards.

Europe's AI buildout is running into a hard constraint: power.

Ukraine, for entirely different reasons, is building the answer.

Europe’s data centre sector consumed roughly 96 TWh in 2024, about 3% of continental demand. Installed capacity sits near 18.7 GW today and is heading toward 36 GW by 2030 on 451 Research projections, a compound annual growth rate of roughly 12%.

The binding constraint is power, not capital. Dublin has operated under a de facto grid-connection cap since 2022, with €5.8 billion of data centre projects stranded for lack of electricity. Frankfurt, Amsterdam and London absorb hyperscaler loads equivalent to one-third to 40% of local demand. Grid connection queues across Western Europe now run 7 to 10 years against construction cycles of about 24 months. The Commission’s January 2026 approval of 10 strategic gigafactory sites, matched by roughly €40 billion in public-private funding, sits on top of this bottleneck.

Ukraine is building a different stack, under fire, for reasons that have nothing to do with AI.

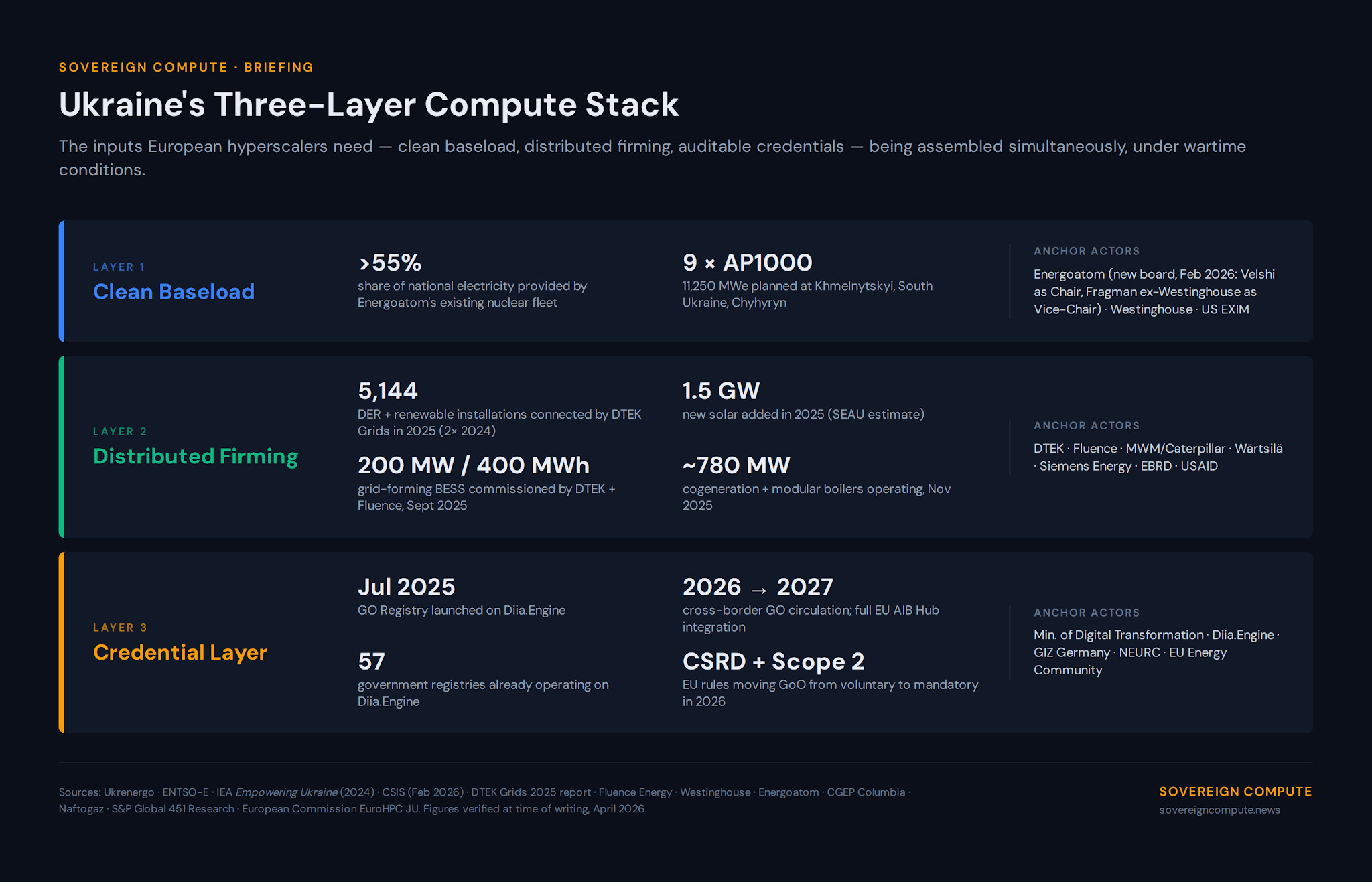

Since the full-scale invasion, roughly two-thirds of Ukraine’s pre-war generating capacity has been damaged, destroyed or occupied. The response has been systematic physical decentralisation. DTEK Grids connected 5,144 distributed generation and renewable installations in 2025, twice the 2024 figure. The Solar Energy Association of Ukraine estimates at least 1.5 GW of new solar was added in 2025, enough for around 1.1 million homes. DTEK and Fluence commissioned 200 MW / 400 MWh of grid-forming battery storage across six dispersed sites in September 2025, the largest such portfolio in the country. The government’s Strategy for the Development of Distributed Generation, approved August 2024, targets 27% of consumption from DERs by 2030. By November 2025 the district heating sector already operated 182 cogeneration units and 239 block-modular boilers providing roughly 780 MW combined, with 500 MW of additional decentralised capacity planned for 2026.

That decentralisation profile - thousands of small, dispersed sources feeding autonomous load pockets - matches what modern AI compute wants: distributed dispatch, resilience to single-point failure, and on-site firming capability. Dublin’s problem is a concentrated 100-MW hyperscale load arriving at a constrained node. Ukraine’s evolving topology is the inverse.

Firming = conversion of variable or intermittent power into reliable, dispatchable power that can match demand at any moment.

Three layers being assembled in parallel: nuclear baseload (Energoatom + AP1000s), distributed firming (DER + BESS + cogeneration), credential layer (Diia.Engine GO Registry).

The baseload layer is being rebuilt in parallel.

Energoatom’s nuclear fleet generates over 55% of national electricity. In July 2025, Westinghouse and Energoatom signed a fuel-assembly partnership at the Ukraine Recovery Conference, advancing the plan to build nine AP1000 reactors: 11,250 MWe of new capacity targeting Khmelnytskyi, South Ukraine, and Chyhyryn. Following the November 2025 corruption scandal, the government appointed a new seven-member supervisory board on 28 January 2026; at its first meeting on 26 February it elected Rumina Velshi (former CEO of the Canadian Nuclear Safety Commission and former Chair of the IAEA Commission on Safety Standards) as Chair, and Patrick Fragman (former President and CEO of Westinghouse Electric) as Vice-Chair. Fragman also chairs the new Strategy and Financial Planning Committee, a direct operational link between Ukraine’s nuclear governance and the technology provider for the AP1000 build.

The credential layer makes the whole thing legible to European buyers. Ukraine launched its Registry of Renewable Energy Facilities on the Diia.Engine platform in July 2025, the same low-code state infrastructure that Germany’s GIZ helped scale into 57 operational government registries and that drew architectural lessons from Estonia’s X-Road. Cross-border circulation of Ukrainian Guarantees of Origin is scheduled to launch in 2026, with full integration into the EU Association of Issuing Bodies by 2027. Under incoming Corporate Sustainability Reporting Directive obligations and the 2026 revision of GHG Protocol Scope 2 guidance, auditable GoO provenance is moving from voluntary to mandatory for European corporates. Hyperscaler contracts increasingly require 24/7 hourly matching, which only a digital registry can verify. The registry is the precondition for procurement-grade clean-compute exports.

Two constraints remain live. Ukraine’s export capacity to the EU is 900 MW as of the ENTSO-E July 2025 revision, and the 2.45 GW cross-border capacity operating in January 2026 is import-weighted during wartime. Ukrenergo’s Recovery Plan targets substantial transfer expansion by 2030, but the lines are not built. And the sector’s political economy - DTEK on distribution, Naftogaz on gas, Energoatom on nuclear - requires parallel governance reform for any compute-export contract to hold. The Fragman appointment suggests Kyiv knows this.

Ukraine has 31 bcm of underground gas storage, the largest in Europe, third globally, currently around 90% full with roughly 10 bcm held on behalf of traders from 21 countries. The country has been operating as Europe’s gas battery for years; the same 21-country counterparty footprint that uses Ukrainian storage as flexibility today is the contractable customer base for clean-compute output tomorrow. For an AI buildout that increasingly demands on-site firming (Cleanview’s February 2026 analysis projects 30% of incremental US data centre capacity from on-site generation in 2026, rising toward 50% - a ratio US-led but increasingly visible across Western European projects), gas storage adjacent to ENTSO-E transfer capacity is a firming reserve that Frankfurt cannot replicate.

For infrastructure investors, the question is whether the EU’s €20 billion InvestAI facility, the EIB’s gigafactory co-financing track, and the World Bank’s roughly $67 billion reconstruction envelope get treated as three separate files or as one. The inputs for a Ukrainian sovereign-compute node are already being assembled by necessity. The financing stacks that would contract the output are still being written.

Sources

· EuroHPC JU — AI Factories and AI Gigafactories

· European Commission — MoU on AI Gigafactories (Dec 2025)

· S&P Global 451 Research — European DC power demand to double by 2030 (Jul 2025)

· ENTSO-E — Go-live of explicit monthly long-term auctions on Ukrainian borders (Dec 2025)

· Ukrenergo — EU import capacity increase to 2.45 GW (Jan 2026)

· IEA — Empowering Ukraine Through a Decentralised Electricity System (Dec 2024)

· CSIS — Striving for Access, Security, and Sustainability (Feb 2026)

· DTEK Grids — 2025 distributed generation connections report

· Fluence Energy / DTEK — 200 MW BESS commissioning (Sept 2025)

· Westinghouse–Energoatom — AP1000 partnership and fuel assembly agreement (Jul 2025)

· Euromaidan Press — Energoatom supervisory board appointments (Jan 2026)

· Ukrainian Energy — Guarantees of Origin registry integration timeline (May 2025)

· CGEP Columbia — Ukraine’s Underused Gas Storage Capacity (May 2025)

· Naftogaz — Underground gas storage business unit

· FP Analytics — Investing in Energy Security: Ukraine (Nov 2025)

· CEPA — A Rebirth in Flame: Ukraine’s Beleaguered Energy System (Dec 2025)

· TechPolicy.Press — Ireland’s data center crisis and EU AI sovereignty (Dec 2025)

A note on independence: All opinions shared in this newsletter are my own and do not reflect the views of dmg events, ADIPEC, or any affiliated organizations. This is personal analysis, not institutional positioning.