What Hormuz Actually Revealed About the AI Stack

The war exposed the Gulf’s dependency on US chips. It also exposed the US’s dependency on Gulf capital. The second vulnerability may matter more.

What happens when the Gulf deploys a form of geopolitical leverage it had not previously used: compute capital?

The consensus formed fast. Within days of Iranian drones striking three Amazon Web Services data centers across the UAE and Bahrain — the first confirmed military attack on hyperscale cloud infrastructure in any conflict — the narrative was set: the Gulf’s sovereign AI ambitions are physically fragile, and anyone building compute infrastructure in the region needs to rethink.

Bloomberg called the Strait of Hormuz “the hidden risk to the AI economy.” Fortune ran the drone strikes as a harbinger of future conflicts. CSIS drew parallels between oil and compute infrastructure as strategic targets. Rest of World mapped the simultaneous closure of both the Strait of Hormuz and the Red Sea to commercial shipping — the first time both data corridors between Asia and Europe have been shut at once. Semafor argued data centers are soft targets that need government-led protection.

The risks are real. But most of the coverage stops at the physical layer — and the more consequential shift is happening one layer down, in capital flows.

The question of whether Gulf data centers can withstand missile strikes is a valid engineering problem that will be addressed. The more consequential question is what happens when the Gulf deploys a form of geopolitical leverage it had not previously used: compute capital.

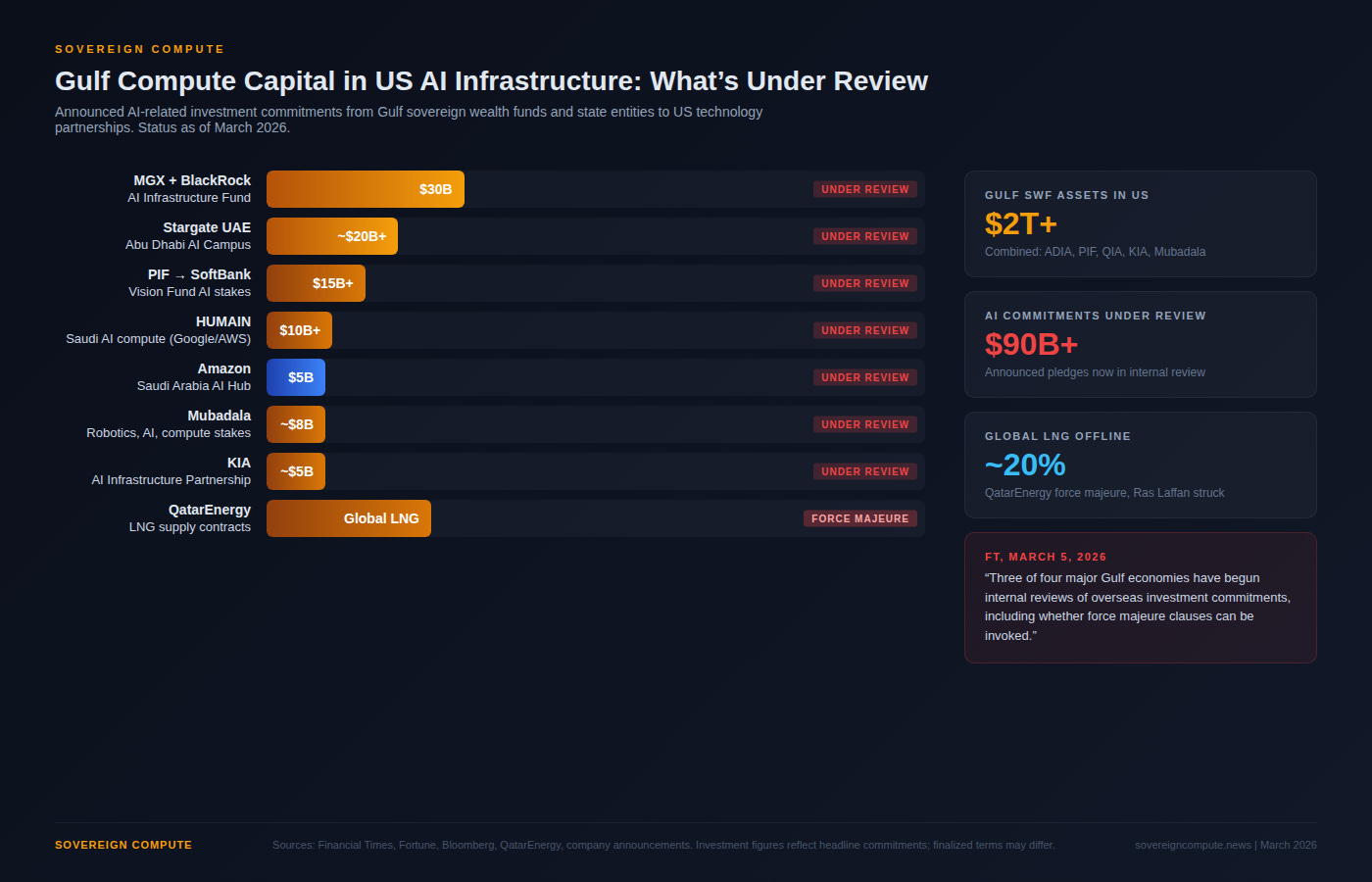

On March 5, the Financial Times reported that three of the four major Gulf economies — Saudi Arabia, the UAE, Kuwait, and Qatar — have begun internal reviews of overseas investment commitments. The review encompasses everything from existing contracts and force majeure clauses to future pledges made to foreign governments and corporations. A Gulf official told the FT the review was driven by converging pressures: declining energy revenues from disrupted exports, surging defense spending, collapsed tourism and aviation, and the sheer cost of intercepting hundreds of Iranian missiles and drones. An adviser to a Gulf government confirmed that the prospect of an investment pullback had already drawn attention inside the White House.

The scale of what is under review matters enormously for AI infrastructure. Gulf sovereign wealth funds collectively hold over $2 trillion in US assets. Following President Trump’s May 2025 regional visit, Saudi Arabia, the UAE, and Qatar pledged hundreds of billions of dollars in new US investments — commitments the White House promoted as validation of its Middle East posture. Those same pledges now sit in limbo. And a substantial share of them was earmarked specifically for AI infrastructure, data centers, and technology partnerships: MGX and BlackRock’s $30 billion AI infrastructure fund, PIF’s investments in SoftBank’s Vision Fund, KIA joining the AI Infrastructure Partnership, Mubadala’s stakes across robotics and compute, the planned Stargate UAE campus in Abu Dhabi, Amazon’s $5 billion Saudi AI hub.

This is structural capital in the US AI buildout, which became conditional.

Before the war started, Foreign Policy published a piece (February 23) arguing that Gulf AI investment in the United States was partly about securing American military protection. The logic was straightforward: sovereign wealth fund capital flowing into US technology created bilateral dependencies that made Washington more invested in Gulf security. It was an insurance premium paid in the form of infrastructure investment.

That deal broke its first real test. The Gulf states hosted US military bases, absorbed Iranian retaliation across their territory, watched drone strikes hit their ports, airports, refineries, hotels, and — for the first time in history — their data centers. The UAE alone intercepted 165 ballistic missiles, 2 cruise missiles, and 541 drones in a single weekend. QatarEnergy declared force majeure on LNG exports after strikes on the Ras Laffan facility, taking roughly 20% of global LNG supply offline. Saudi Arabia’s Ras Tanura refinery, processing 550,000 barrels per day, was hit by Iranian drones.

The investment review carries a political charge that extends well beyond budget management. QatarEnergy’s CEO Saad al-Kaabi was blunt in comments to the Financial Times: “Everybody that has not called for force majeure we expect will do so in the next few days that this continues. All exporters in the Gulf region will have to call force majeure. If this war continues for a few weeks, GDP growth around the world will be impacted.” The force majeure applies to delivery windows, not the long-term supply contracts themselves — a distinction that triggers different insurance clauses and changes the risk calculus for counterparties.

If Gulf sovereign wealth funds slow new commitments to US technology — or publicly invoke force majeure on existing contracts — the reverberations will reach every AI infrastructure deal structured around Gulf capital. The war exposed the Gulf’s dependency on US chips, which was already well understood. It simultaneously exposed the US’s dependency on Gulf capital, which was not. Hormuz made both visible at the same time.

The Physical Layer and the Economic Layer

The dominant narrative treats the Hormuz crisis as evidence that the Gulf’s sovereign AI model is broken. It isn’t. The model is stressed, and the connectivity layer is genuinely exposed. But the structural economics that made the Gulf attractive for AI infrastructure have not changed.

Electricity in Abu Dhabi still costs roughly $0.05 per kilowatt-hour, versus $0.09–$0.15 in Virginia. Both the UAE and Saudi Arabia have bypass pipelines for oil exports — the Abu Dhabi Crude Oil Pipeline to Fujairah, the Saudi East-West Pipeline — that can move part of the crude outside the Strait of Hormuz. Sovereign capital still does not require quarterly earnings calls. Permitting timelines measured in months, not years. These advantages do not disappear because of a conflict. They are why the Gulf attracted over $2 trillion in AI-related investment pledges in the first place.

Data centers are no more inherently vulnerable to ballistic missiles than oil refineries, desalination plants, or petrochemical complexes — all of which Gulf states have defended as critical national infrastructure for decades. The AWS drone strikes are an engineering and defense problem that will be solved the way Gulf states have solved similar problems for their energy infrastructure. Fortune reported that the US military used Anthropic’s Claude model, running on AWS infrastructure, for intelligence assessments and target identification during the Iran strikes. Iran’s Fars News Agency cited this dual-use reality as justification for targeting the Bahrain data center. The boundary between commercial cloud and military operations has collapsed — and that changes the threat model for every data center in a contested region. But it also changes the defense priority. Gulf states will now treat data center protection with the same urgency they apply to oil terminals and desalination plants.

The connectivity disruption from subsea cable exposure is a real vulnerability — but it is a connectivity vulnerability, separate from the compute capacity question. If anything, it validates the case for localized compute infrastructure rather than serving the Middle East and South Asia from data centers in Virginia. The organizations that bet on remote service delivery to one of the world’s fastest-growing AI markets are the ones most disrupted by the simultaneous closure of both maritime data corridors.

Who Is Actually Exposed

The Hormuz crisis reveals remote dependencies more starkly than local ones. Consider who has actually been hit hardest.

Bloomberg reported that more than half the world’s DRAM and NAND memory chips are manufactured in South Korea, and approximately 70% of advanced processing chips are made in Taiwan. Both countries are among the most dependent on Qatari LNG flowing through Hormuz. South Korea’s KOSPI crashed 12% in a single session — the largest drop since 2008 — with SK Hynix down 14.5%, hit harder than Samsung due to its higher reliance on specialized neon gas precursors that transit through the Strait. Taiwan holds less than a month of LNG reserves. Qatar alone accounts for roughly 30% of Taiwan’s LNG shipments. TSMC, which fabricates about 90% of the world’s cutting-edge semiconductors, consumes nearly 9% of Taiwan’s total electricity supply.

The implication is direct: the organizations that assumed they could serve the global AI buildout from fabs in East Asia powered by Gulf LNG are watching their energy supply chain fracture in real time. Taiwan’s gas reserves would last roughly ten to eleven days under normal consumption. Once ships currently en route discharge their cargoes, any ongoing disruption at Hormuz bites directly into the electricity supply powering the fabs that produce the world’s most advanced chips. The Thai stock exchange triggered its circuit breaker on an 8% drop. Asian jet fuel prices surged approximately 200%.

Europe’s exposure is no less severe. Natural gas prices nearly doubled within 48 hours of Hormuz closing. Germany’s wholesale electricity prices, already the highest among major economies, spiked further. The EU faces a reprise of its 2022 energy crisis, but this time with depleted winter gas storage. France (nuclear) and the Nordics (hydro) are partially insulated. The rest of the continent is not. Every European AI data center running on gas-fired electricity just got more expensive to operate.

The Hormuz crisis is a stress test of every jurisdiction’s energy assumptions. The jurisdictions that look most fragile are the ones furthest from the headlines.

Why Single-Layer Risk Analysis Fails

Most analysis of sovereign AI infrastructure collapses multiple, distinct risk layers into a single assessment. “Gulf AI: risky” is a headline, and headlines make poor investment frameworks.

Physical infrastructure resilience is one layer. Connectivity is another. Model and chip dependency is another. Regulatory sovereignty is another. Capital flows are yet another. The Hormuz crisis demonstrates why treating these as a single variable produces bad analysis. The Gulf’s energy and capital advantages remain structurally intact. Its connectivity layer is genuinely exposed. Its dependency on US chips and models was a known vulnerability before any missiles flew. And the bilateral trust relationship with Washington — the foundation of chip export approvals, the AI Acceleration Partnership, and the entire Gulf sovereign AI strategy — has been challenged, because the security assumption underlying the partnership failed its first real trial.

The Forward Signal

Whether this war lasts weeks or months, the compute capital dynamic is now visible and will not be forgotten. The Gulf states now understand that their AI infrastructure investment in the United States doubles as a geopolitical instrument. The US now understands that its AI infrastructure buildout carries a sovereign capital dependency it had not stress-tested. Neither side had priced this bilateral vulnerability before Hormuz. Both sides will price it from now on.

The practical consequences are already materializing. Every AI infrastructure partnership structured as “Gulf capital in exchange for US technology access” now carries a new risk premium. The chip export approvals that underpinned the Gulf’s AI strategy — the deal that let G42 divest Chinese holdings in exchange for NVIDIA access, the framework that gave HUMAIN its initial Blackwell allocation — are still technically in force. But the trust layer beneath them has been questioned. Regulatory approvals and commercial contracts assume stable bilateral relationships. When the bilateral relationship is under strain, every approval and every contract becomes contingent in ways that the original terms did not anticipate.

For anyone making deployment, investment, or regulatory decisions in the AI infrastructure space, a new question has joined the familiar ones about chips and electricity costs: who funds the stack — and what happens when that funding becomes conditional?

Sources

Financial Times (March 5, 2026): Gulf states reviewing investment commitments and force majeure clauses

Fortune (March 9, 2026): Iranian drone strikes on Amazon data centers — first deliberate targeting of data centers in conflict

Fortune (March 3, 2026): AWS confirms structural damage to UAE and Bahrain facilities

Bloomberg (March 5, 2026): “Hormuz Is the Hidden Risk to the AI Economy” — LNG dependency of chip fabs

Rest of World (March 5, 2026): Simultaneous closure of Hormuz and Red Sea; hyperscaler infrastructure at risk

Semafor (March 3, 2026): Data centers as soft targets requiring government-led protection

CSIS (March 3, 2026): “If Compute Is the New Oil” — parallels between oil and compute infrastructure

Foreign Policy (February 23, 2026): Gulf AI investment as partly about US military protection

CNBC (March 4, 2026): IRGC claims deliberate targeting of AWS Bahrain for military support role

CNBC (March 3, 2026): Banking and payments disruptions across UAE from AWS outages

QatarEnergy: Force majeure declaration on LNG shipments following Ras Laffan strikes

Khalaf Al Habtoor: Public criticism of Trump on X (March 5, 2026)

Tom’s Hardware (March 7, 2026): Uptime Institute confirms first military attack on hyperscale cloud provider

A note on independence: All opinions shared in this newsletter are my own and do not reflect the views of dmg events, ADIPEC, or any affiliated organizations. This is personal analysis, not institutional positioning.