THREE MODELS OF SOVEREIGN AI

And the blind spot each architect has not fully tackled

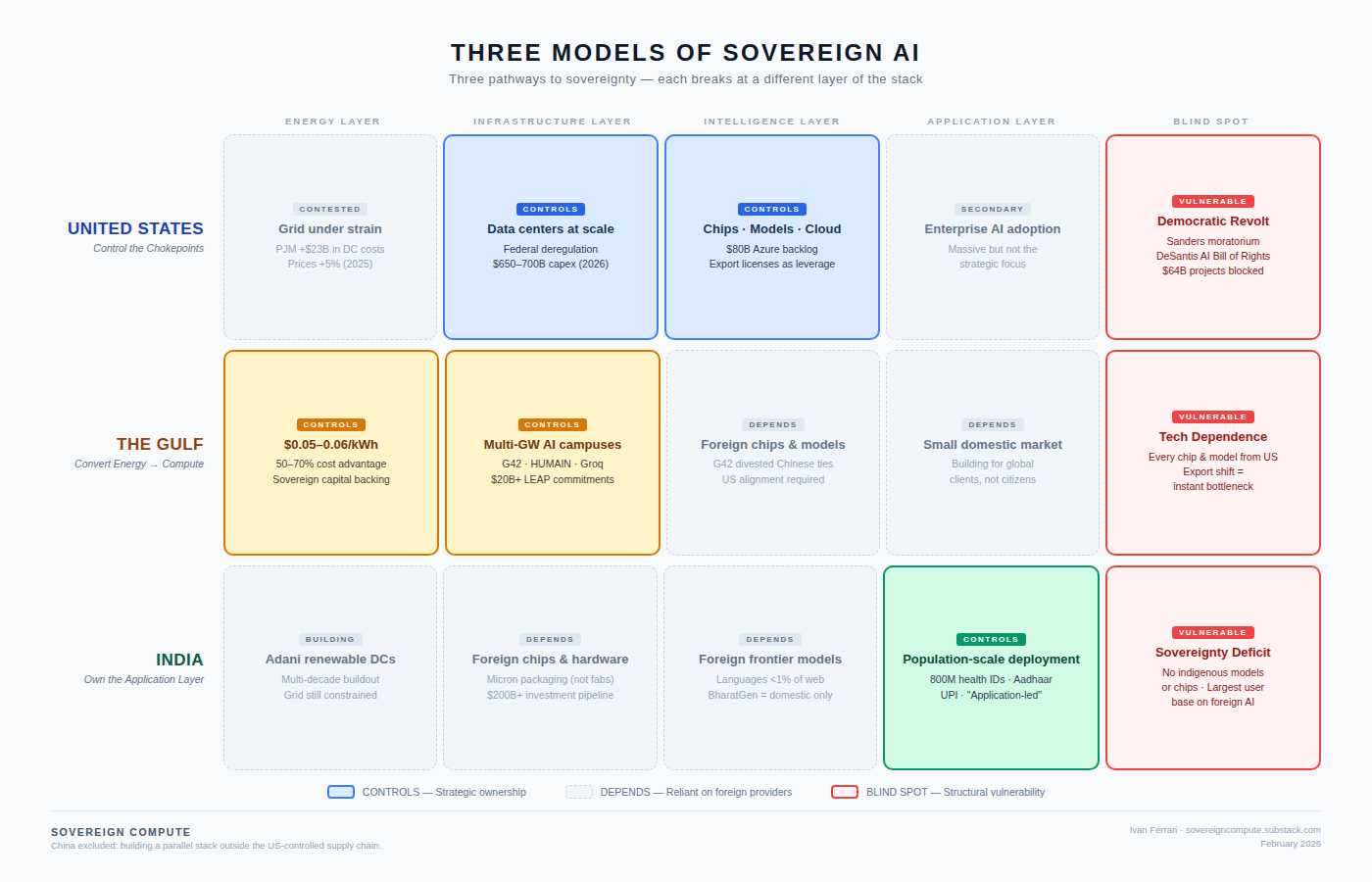

Every major economy now treats AI infrastructure as a strategic asset on par with energy reserves or nuclear capability. But agreement on the destination has produced three radically different routes to get there. The United States, the Gulf states, and India are each constructing sovereign AI ecosystems built on fundamentally different theories of power — and each model contains a structural blind spot its architects would rather not discuss.

China is conspicuously absent from this analysis — not because it doesn’t matter, but because it’s playing a different game entirely. Beijing is building a parallel AI stack outside the US-controlled supply chain, forced by export controls into a self-sufficiency model that deserves its own treatment. This piece focuses on the three major models competing within the US-anchored ecosystem — because that’s where the infrastructure capital, the energy bottlenecks, and the policy contradictions are most acute right now.

The American Model: Control the Chokepoints

The US doesn’t build sovereign AI infrastructure the way other countries do. It doesn’t need to. American sovereignty comes from controlling the supply chain itself: the chips, the cloud platforms, the foundation models, and the export licenses that determine who else gets access. NVIDIA, Microsoft, Google, Amazon, and Meta are projected to spend on the order of $650–700 billion in capex in 2026, with the majority tied to AI infrastructure. Hyperscaler earnings make clear the market is supply-constrained, not demand-constrained. Microsoft disclosed an approximately $80 billion backlog of Azure orders it cannot fulfill because there isn’t enough power.

Sources: Introl hyperscaler capex analysis (Jan 2026); MacroNotes analysis of Microsoft Azure backlog.

The Trump administration has turned this into explicit policy. Through executive action in January 2025 — revoking Biden’s AI safety executive order (EO 14110) and replacing it with “Removing Barriers to American Leadership in Artificial Intelligence” (EO 14179) — and a sweeping December 2025 order (“Ensuring a National Policy Framework for Artificial Intelligence”) preempting state-level AI regulation, the administration has framed sovereignty as deregulation. The December order directs the Attorney General to establish an AI Litigation Task Force within 30 days to challenge state AI laws deemed inconsistent with federal policy. It instructs the Secretary of Commerce to condition remaining broadband deployment (BEAD) funds on states not having “onerous” AI laws. The message is clear: the federal government will clear the runway for private capital to build at scale, and use export controls to decide who else gets to play.

Sources: Mayer Brown analysis (Dec 23, 2025); Squire Patton Boggs analysis (Jan 2025); Utility Dive (Dec 8, 2025).

The blind spot: the people who live next to the runways are revolting

A populist backlash is brewing across red and blue states alike. Senator Bernie Sanders endorsed a national moratorium on data center construction in December 2025, likely the first member of Congress to do so, citing concerns about the unregulated growth of AI and its impact on employment. Governor Ron DeSantis announced a proposed AI Bill of Rights on December 4, 2025, including provisions that would prohibit utilities from charging Florida residents more to support hyperscale data center development and allow local governments to block data center construction. In Wisconsin, the mayor of Port Washington faced a recall campaign after approving a $15 billion data center for OpenAI and Oracle through the Stargate project. In the PJM Interconnection — the grid serving 67 million people across 13 states — data center demand added over $23 billion to capacity auction costs across three consecutive auctions, costs that flow directly to consumers. According to Data Center Watch, $64 billion in data center projects were blocked or delayed through early 2025 by local bipartisan opposition. Residential electricity prices rose approximately 5% in 2025 and are forecast to climb another 4% in 2026, according to the federal Energy Information Administration. With mid-term elections in November, data center opposition is becoming a bipartisan campaign issue.

Sources: E&E News/Politico (Dec 17, 2025); Florida Governor press release (Dec 4, 2025); Wisconsin Watch/Racine County Eye (Jan 2026); Bloomberg/Monitoring Analytics (Jan 5, 2026); CNBC (Jan 1, 2026); EIA electricity price forecast.

The paradox is sharp: the administration that removed every federal barrier to AI buildout may find the real barrier is voters.

The Gulf Model: Convert Energy Wealth into Compute Wealth

Saudi Arabia and the UAE are running a different playbook. Where the US controls the supply chain, the Gulf is investing its way into the infrastructure layer — fast, at scale, and with sovereign capital that doesn’t need quarterly earnings calls.

The headline commitments are staggering. G42 and partners have announced plans for a multi-gigawatt UAE-US AI Campus in Abu Dhabi, with an initial 1GW phase breaking ground. Microsoft committed billions to the UAE through 2029. Saudi Arabia’s HUMAIN has announced plans to deploy substantial compute capacity by 2030, beginning with an initial allocation of Nvidia Blackwell chips. At a business event in 2025, Saudi Arabia attracted over $20 billion in headline investment commitments, including Groq’s announced plans for a major inference data center.

Note: Gulf investment figures represent headline commitments and announced plans; finalized deal terms may differ.

The structural advantage is deceptively simple: typical Gulf electricity costs run approximately $0.05–0.06 per kilowatt-hour versus $0.09–0.15 in the US. At data center scale, that 50–70% energy cost advantage compounds into an operating margin moat. The Gulf is essentially doing what it did with petrochemicals in the 1980s: converting a natural resource advantage (cheap energy) into downstream industrial capacity (compute), backed by state capital.

Source: Euro-Security analysis of AI infrastructure economics (2026).

Governments don’t just enable this buildout — they orchestrate it. The UAE was the first country to appoint a Minister of State for Artificial Intelligence, in 2017. Abu Dhabi established the Artificial Intelligence and Advanced Technology Council. Saudi Arabia’s SDAIA coordinates national AI strategy under Vision 2030. Neither country has a standalone AI law, but both govern through a layered approach — data protection, ethics charters, cybersecurity rules, and sector-specific guidance — that gives the state flexibility to adjust without locking in rigid frameworks. The UAE’s approach has been described as a “sandbox state”: policy precedes statute, enabling rapid iteration.

The blind spot: technological dependence

Every advanced chip, every foundation model, every cloud operating system comes from the US or (to a lesser extent) China. When the Trump administration approved advanced AI chip exports to the UAE and Saudi Arabia, it attached strict security requirements and reporting obligations. G42 divested its Chinese investments — including a reported stake in ByteDance — under US national security pressure. The Gulf’s AI sovereignty is real at the infrastructure layer but fragile at the intelligence layer. If export policy shifts, or if US-China competition forces harder choices about alignment, the Gulf’s compute campuses could face the same bottleneck that constrains their clients: access to the models and chips that make the hardware useful.

Sources: Multiple reporting on G42 divestment from Chinese investments under US pressure (2024–2025).

Citizens in the Gulf, meanwhile, aren’t pushing back — partly because energy is heavily state-subsidized and electricity costs are largely invisible to households, and partly because the state-led model doesn’t create the community-level disruptions that American data centers do. There are no recall campaigns in Abu Dhabi.

The Indian Model: Own the Application Layer

India’s play is the most counterintuitive. While the US controls the supply chain and the Gulf builds the hardware, India is betting that owning the application layer — deploying AI at population scale — matters more than owning the models or the chips.

The India AI Impact Summit made the strategy explicit. Adani Group announced plans for a massive, multi-decade investment in renewable-powered AI data centers. The Indian government expects over $200 billion in AI investment across the full stack in the coming years. Google, Microsoft, Amazon, OpenAI, and Anthropic all sent their CEOs to New Delhi. India has earmarked roughly $1 billion for an AI-focused venture capital fund. Micron is establishing semiconductor packaging and test operations in Gujarat.

Note: Indian investment figures represent government projections and corporate announcements; actual deployment timelines may vary.

But India has consciously chosen not to chase frontier model development. The country’s Economic Survey has urged a focus on application-led innovation rather than competing on foundation models. As Infosys chairman Nandan Nilekani has said, the approach is essentially: let the major US labs build the frontier models, and India will use them to create synthetic data, build smaller language models, and deploy AI at scale using locally relevant data. India’s AI startup funding remains a small fraction of US investment. Domestic model efforts like BharatGen are focused on Indian-language capabilities for domestic deployment, not frontier competition.

India’s governance approach mirrors this philosophy. The AI Governance Guidelines are principle-based and explicitly pro-innovation. There’s no standalone AI law. The government’s posture is clear: don’t regulate what you want to grow.

The blind spot: the largest sovereignty deficit in the global AI race

India is building the world’s largest AI deployment infrastructure while remaining entirely dependent on foreign models and foreign chips. Indian languages comprise less than 1% of global web content, making frontier model training structurally difficult. Indian venture capital demands commercial returns too fast for the long, capital-intensive model-building cycle. And India’s digital public infrastructure — 800 million health IDs, the Aadhaar biometric system, the UPI payments network — creates an application surface that is unmatched globally but also creates enormous data governance risks if the intelligence layer is controlled abroad.

Indian citizens, for their part, are the most engaged of the three models — but in a paradoxical way. India has among the largest ChatGPT user bases in the world. They are enthusiastic adopters of foreign AI. Civil society, meanwhile, is raising alarms about how AI tools may be used for surveillance and political targeting. India’s public is simultaneously the world’s most eager consumer of AI and among the most exposed to its governance failures.

The Strategic Question

Each model optimizes for a different layer of the stack. The US controls the intelligence layer and the supply chain but faces a democratic revolt over the physical layer. The Gulf controls the infrastructure layer but depends on the US for everything that runs on it. India is building the application layer at a scale no one else can match but has no indigenous control over the models or the hardware beneath it.

The question for infrastructure investors, energy executives, and policy strategists is not which model is right. It’s which model survives a supply chain shock — a chip export ban, an energy price spike, a regulatory reversal. The US model is most vulnerable to its own citizens. The Gulf model is most vulnerable to the USA’s foreign policy. The Indian model is most vulnerable to the models it doesn’t own.

The sovereign AI race isn’t a single competition. It’s three parallel experiments in what “control” means in an era when intelligence is becoming infrastructure. The results will reshape energy markets, capital flows, and geopolitical alliances for the next generation. And none of the three architects has solved the full puzzle yet.

EDITORIAL NOTE

This analysis represents the author’s interpretive framework. The “three models” taxonomy and “blind spot” assessments are analytical constructs, not formal categories used by the governments discussed. Gulf and Indian investment figures reflect headline announcements and government projections; finalized commitments may differ. China’s parallel sovereign AI stack — including domestic chips (Huawei Ascend), foundation models (DeepSeek, Qwen), and cloud platforms — is excluded here because it operates outside the US-anchored supply chain ecosystem analyzed in this piece and warrants separate treatment.

Looking forward to checking out more of your post in the future

This is good stuff. First time I've seen it. Keep it up.