The War isn't slowing the AI buildout, but it changes the coordinates, capital sources,and who controls the stack.

What Breaks When Oil Hits $180 and Data Centers Are Hit?

Twenty days into the US-Iran conflict, the Strait of Hormuz is effectively closed. Oman crude hit $167 per barrel on the Gulf Mercantile Exchange on March 19, with physical delivery premiums in Asia pushing transaction prices even higher. Brent futures, at roughly $110, trail by over $50—a paper-versus-physical gap that normally runs $5–8 and that itself signals how dislocated energy markets have become. Iranian drones have struck three AWS data centers in the UAE and Bahrain—the first confirmed military attacks on hyperscale cloud infrastructure in history. And as of March 18, the conflict escalated from logistics disruption to infrastructure destruction: Israeli strikes targeted South Pars, the Iranian side of the world’s largest natural gas field, whose Qatari counterpart—North Field—feeds Ras Laffan, the single largest LNG export facility on Earth. Blocked shipping lanes reopen when wars end, but damaged production infrastructure does not.

The instinct is to ask whether all of this slows the AI buildout. The critical question is which layers of the AI stack break under a sustained energy shock—and which accelerate because of it. On the software layer, the answer is unambiguous. The US military struck over 1,000 targets in the first 24 hours of Operation Epic Fury using Palantir’s Maven system integrated with AI for real-time targeting. Palantir stock is up 12% since the campaign began, its US government revenue having grown 55% year-over-year to $1.9 billion in 2025. In parallel, Bloomberg reported this week that Maxence Visseau, founder of investment firm Arkevium, used AI to cut research time by roughly 80%, stress-testing conflict scenarios across asset classes in minutes. When a CFO faces Oman crude above $165 and Brent above $110, compressing margins and spiking input costs, the business case for AI-driven efficiency stops being aspirational.

The hardware layer faces a different calculus. The Middle East AI buildout—one of the fastest-growing in the world through 2025—is obviously stalling. CSIS analysts now frame data centers as legitimate military targets in modern armed conflict. Pure Data Centre Group’s CEO told CNBC his firm would “slow down” in the region. The Atlantic Council’s Tess deBlanc-Knowles notes the Gulf remains attractive for its sovereign capital, energy, and Global South market access—but hyperscalers are running scenario analyses on redirecting next-wave capacity to Northern Europe, India, and Southeast Asia. This is geographic redistribution, though, not aggregate reduction. The CapEx still flows.

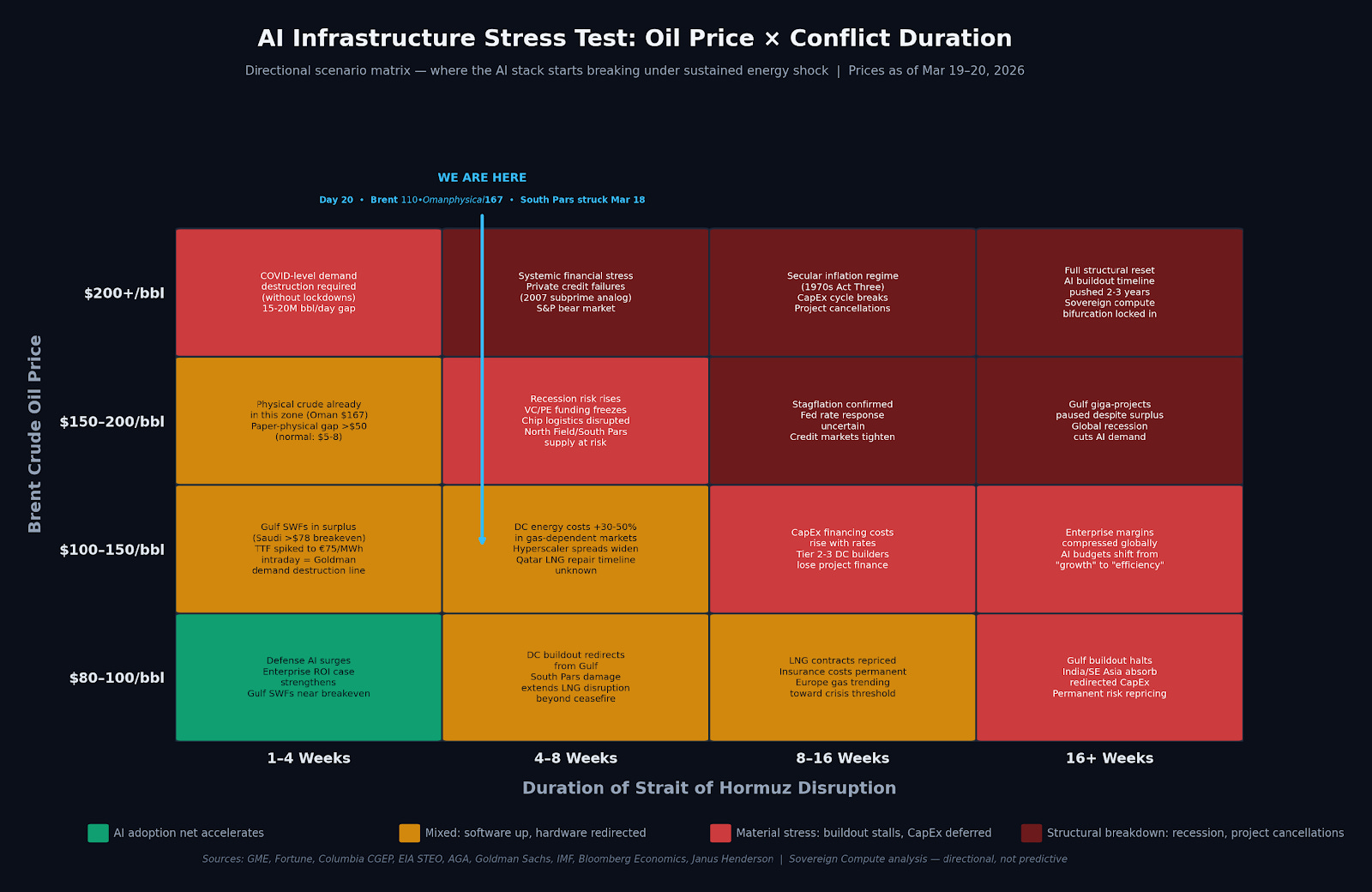

The stress-test matrix above maps where specific AI stack components begin to fracture, plotted against oil price and conflict duration. The thresholds are directional, anchored to observable data. Saudi Arabia’s fiscal breakeven sits at $78–94 per barrel depending on whether PIF spending is included (IMF, Bloomberg Economics), meaning Gulf sovereign wealth funds are currently generating windfall surpluses of $49–72 billion annualized. Goldman Sachs estimates European gas at €74/MWh would replicate 2022-level demand destruction. On March 18, TTF spiked to $24/MMBtu—approximately €75/MWh—touching Goldman’s crisis threshold intraday before settling lower, with Brent at $109. TTF has since traded in the €50–67/MWh range, trending toward the crisis line as South Pars damage compounds.

The direction matters more than any single close. Energy constitutes 15–25% of data center operating costs at baseline—but the South Pars escalation changes the timeline. Production infrastructure damage means LNG supply disruption persists beyond any ceasefire, repricing gas-dependent data center markets in Asia and Europe on a horizon measured in quarters, not weeks. Columbia’s Center on Global Energy Policy described March 18 as the moment the war moved “from logistical disruption to meaningful and potentially longer-lasting damage to core energy infrastructure assets.”

Duration remains the critical variable, but the South Pars strike has compressed the escalation curve. At three weeks with only shipping disruption, this was a market shock with geographic reshuffling. With production infrastructure now damaged, some portion of the LNG supply hit is locked in regardless of diplomatic outcomes. Extend the conflict to eight or sixteen weeks and the 1970s secular inflation analog—what Bloomberg’s Simon White calls “Act Three”—begins repricing every energy-linked asset class. Janus Henderson is already flagging that hyperscaler credit spreads, which started widening in Q3 2025, still don’t reflect the historical pattern where large debt-funded CapEx cycles produce meaningful spread widening.

The fertilizer disruption—roughly a third of global supply transits the Gulf—introduces a second-order food inflation channel that most AI infrastructure analyses ignore entirely. Several energy strategists, including Rystad and Financial Sense, frame the current disruption as the front edge of a structural energy supply cycle extending to 2030—which means this matrix is less a war-duration exercise than a preview of the operating environment for the next generation of AI infrastructure buildout.

For sovereign compute, the structural implication is clear. The gap between countries with installed AI infrastructure and those still building is widening in real time. The US benefits from its massive installed base and insulated domestic gas prices—Henry Hub near $3/MMBtu while Asian JKM trades above $20. India and Southeast Asia benefit as redirected buildout destinations. The Gulf states face a paradox: their sovereign capital has never been stronger, but the physical security case for hosting critical compute has weakened. Every government watching this conflict—from Brasília to Jakarta to Nairobi—is drawing the same conclusion: domestic compute capacity is a national security requirement, not a commercial preference. The war doesn’t slow the AI transition. It sorts who controls it.

Sources

• Columbia Center on Global Energy Policy, “Iran Conflict Brief: The High Cost of Attacking Energy Infrastructure,” March 20, 2026

• Gulf Mercantile Exchange (GME), Oman Crude OQD Marker Price, March 19, 2026 ($166.96/bbl)

• Fortune, “Oil prices hit nearly $110 as Iran vows to escalate the war,” March 18, 2026

• MacroVoices Episode #524, March 19, 2026

• EIA Short-Term Energy Outlook, March 10, 2026 (Brent $94/bbl as of March 9)

• CNBC, “How the Iran war could impact hyperscalers’ massive AI buildout in the Middle East,” March 11, 2026

• The Hill, “Iran war casts shadow over Middle East AI investments,” March 17, 2026

• Morgan Stanley, “AI Capex and the Iran War: Market Investing Risks,” March 2026

• Goldman Sachs, LNG supply and European gas price analysis, March 3, 2026

• Bloomberg, “Traders Overwhelmed by Iran News Are Turning to AI for Help,” March 19, 2026

• Janus Henderson, “How to play the AI mega-theme in fixed income,” March 2026

• IMF and Bloomberg Economics, Saudi Arabia fiscal breakeven estimates

• American Gas Association, Natural Gas Market Indicators, March 19, 2026

• CNBC, “Middle East war sends natural gas prices soaring,” March 3, 2026

• The Middle East Insider, “Saudi Arabia Economy March 2026,” March 14, 2026

• Rystad Energy, energy infrastructure supply chain analysis, March 2026

• Financial Sense, “Geopolitical Risk and Energy Infrastructure,” March 2026

A note on independence: All opinions shared in this newsletter are my own and do not reflect the views of dmg events, ADIPEC, or any affiliated organizations. This is personal analysis, not institutional positioning.