Southeast Asia Is the Only Place Where the US and China Are Fighting for AI Infrastructure on the Same Soil

The region’s $50 billion data center buildout is the closest thing the AI era has to a contested frontier — and neither superpower controls the rules.

In every other theater of the AI infrastructure race, the lines are drawn.

The US controls its domestic stack. China is building a parallel one. The Gulf buys into the American ecosystem under strict export conditions. India bets on applications over models.

But Southeast Asia — 700 million people, six fast-growing digital economies, and a region where binding AI regulation has only just begun to emerge in Vietnam, leaving the rest as a high-speed, non-binding laboratory — is the one place where American and Chinese hyperscalers are building data centers side by side, competing for the same customers, on the same grids, under the same loose rules.

This is not a metaphor.

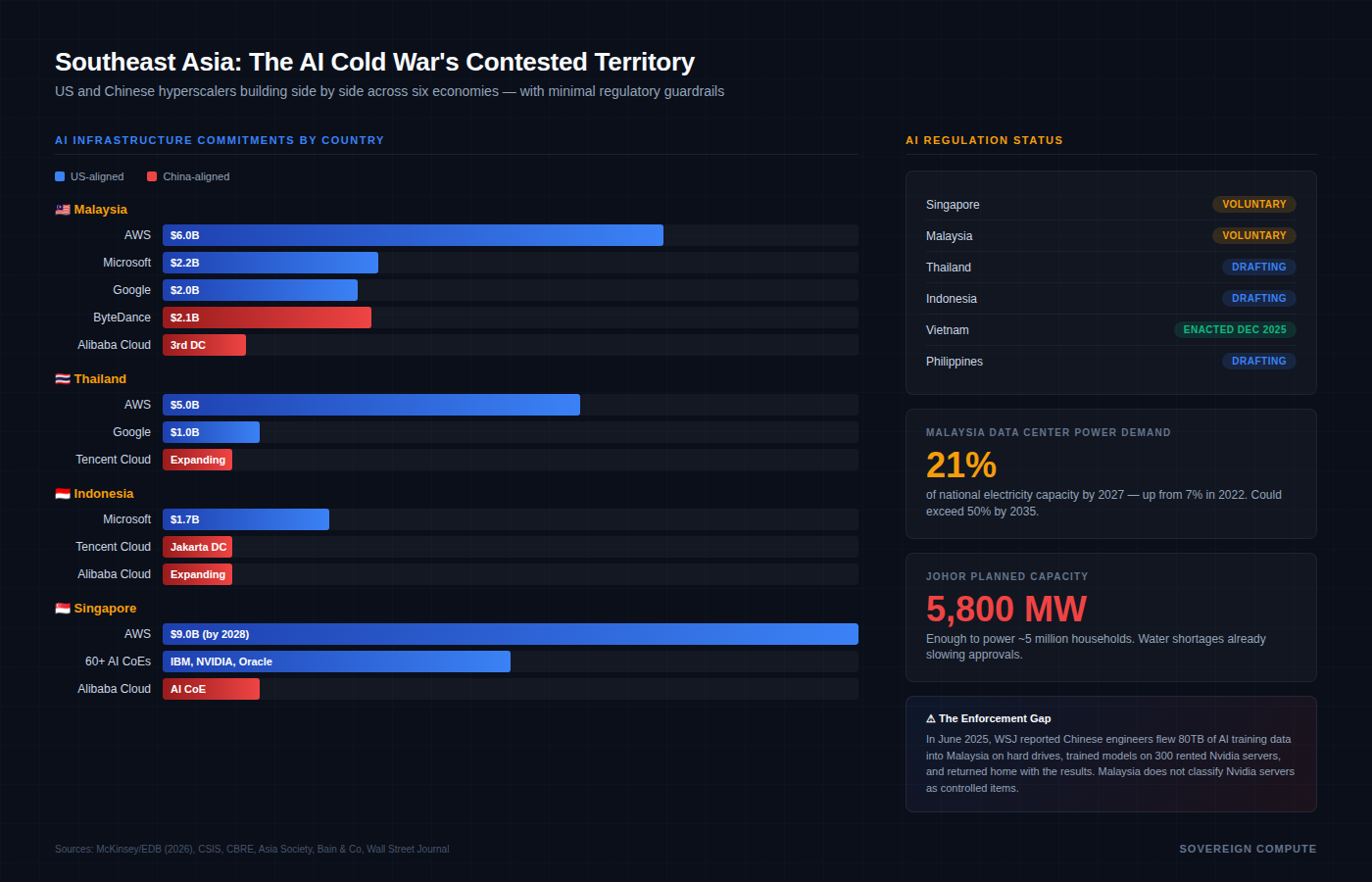

AWS, Microsoft, and Google have collectively committed over $50 billion to the region. Alibaba Cloud, Tencent Cloud, and ByteDance are building alongside them — ByteDance alone has earmarked $2.1 billion for an AI hub in Malaysia’s Johor state, where it is anchor tenant at Bridge Data Centres’ 110MW hyperscale facility. GDS International, a Singapore-listed subsidiary of a Chinese parent, reports that roughly 70% of its Southeast Asian client mix is Chinese.

These figures still look modest against the $600-plus billion in projected 2026 hyperscaler capex globally — but that comparison is misleading. Roughly half of US hyperscaler spend is a check to Nvidia and TSMC for silicon; it never touches local soil. The billions landing in Southeast Asia are steel, concrete, and power connections — permanent infrastructure with a local GDP impact orders of magnitude higher per dollar than a GPU purchase order routed through Santa Clara.

The region is absorbing both stacks simultaneously, and no one is forcing a choice. Indonesia’s Tokopedia runs its live video and data analytics on Google Cloud while its core transactional infrastructure sits on Alibaba Cloud data centers in Jakarta, and in 2024, TikTok reentered the Indonesian market through a merger with Tokopedia itself. One company, both cloud stacks, both superpowers’ consumer platforms, no regulatory friction.

The structural reason is regulatory.

ASEAN’s Guide on AI Governance and Ethics, updated in January 2025 to cover generative AI, is non-binding. No Southeast Asian country had a binding AI law until Vietnam passed one in December 2025. Malaysia, Thailand, and Indonesia are all drafting frameworks, but none have enacted hard regulations. For hyperscalers, that translates to speed: faster permitting, fewer compliance layers, no equivalent of the EU AI Act’s risk classifications. For geopolitical strategists, it translates to something else — a theater where export controls are structurally difficult to enforce.

The evidence is already here. The Wall Street Journal reported in June 2025 that four Chinese engineers flew from Beijing to Kuala Lumpur carrying suitcases packed with 60 hard drives — 80 terabytes of AI training data — and trained models on 300 rented Nvidia servers at a Malaysian data center.

Malaysia does not classify Nvidia-powered servers as controlled items under its Strategic Trade Act. CSIS noted that the performance gap between the best US and Chinese AI models shrank from 9.3% in 2024 to 1.7% by early 2025. Southeast Asia’s under-regulated data centers may be accelerating that convergence — particularly after DeepSeek-R1’s January 2025 release demonstrated that frontier-competitive models could be trained on far fewer GPUs, making the suitcase-and-rented-server approach more viable than ever.

The energy math compounds the stakes. Malaysia’s data center power demand is projected to hit 21% of national electricity capacity by 2027, a massive leap from 7% in 2022, according to Bain & Co. By 2035, the government warns this could exceed 50% of the Peninsular grid’s total capacity. Johor state alone has 5,800MW of planned capacity — enough to power nearly 5 million households. The national grid is 92% fossil fuel. Malaysia has imposed new power tariffs on large data centers, and water shortages in Johor and Selangor have already forced authorities to slow approvals.

For Pax Silica signatories — Singapore, the UAE, and now India are all members — the implications are direct. Singapore has announced tranches aimed at expanding beyond its current 1.4GW data center base, pushing larger requirements to neighboring Malaysia. The Johor-Singapore Special Economic Zone creates passport-free travel between the two, effectively extending Singapore’s digital economy into Malaysian power grids.

Southeast Asia is not a sideshow in the sovereign compute race. It is the contested middle ground — the one place where both superpowers are building, both regulatory models coexist, and the energy constraints haven’t yet forced a reckoning. Infrastructure investors reading Pax Silica as a neat division of the world into blocs should look more carefully at Johor. The blocs overlap there. And the grid is already groaning.

Sources: McKinsey/EDB “AI in Southeast Asia” (Feb 2026); Bain/Google/Temasek “e-Conomy SEA” (2025); CSIS “Cloud Computing in Southeast Asia and Digital Competition with China” (Oct 2024); CSIS “Beyond the Matrix: AI Governance Gaps in Southeast Asia” (2025); Wall Street Journal (Jun 2025); CNBC Johor data center investigation (Aug 2025); Asia Society Policy Institute (Jan 2026); CBRE Asia Pacific Data Centre Outlook (2026); ISEAS-Yusof Ishak Institute (Feb 2026); Crowell & Moring ASEAN Digital Ministers analysis (2026).

A note on independence: All opinions shared in this newsletter are my own and do not reflect the views of dmg events, ADIPEC, or any affiliated organizations. This is personal analysis, not institutional positioning.