Europe Is Paying to Switch Off the Power Its AI Needs

Germany and Spain set record negative-price hours in 2025 while Brussels says it lacks the energy to build frontier compute.

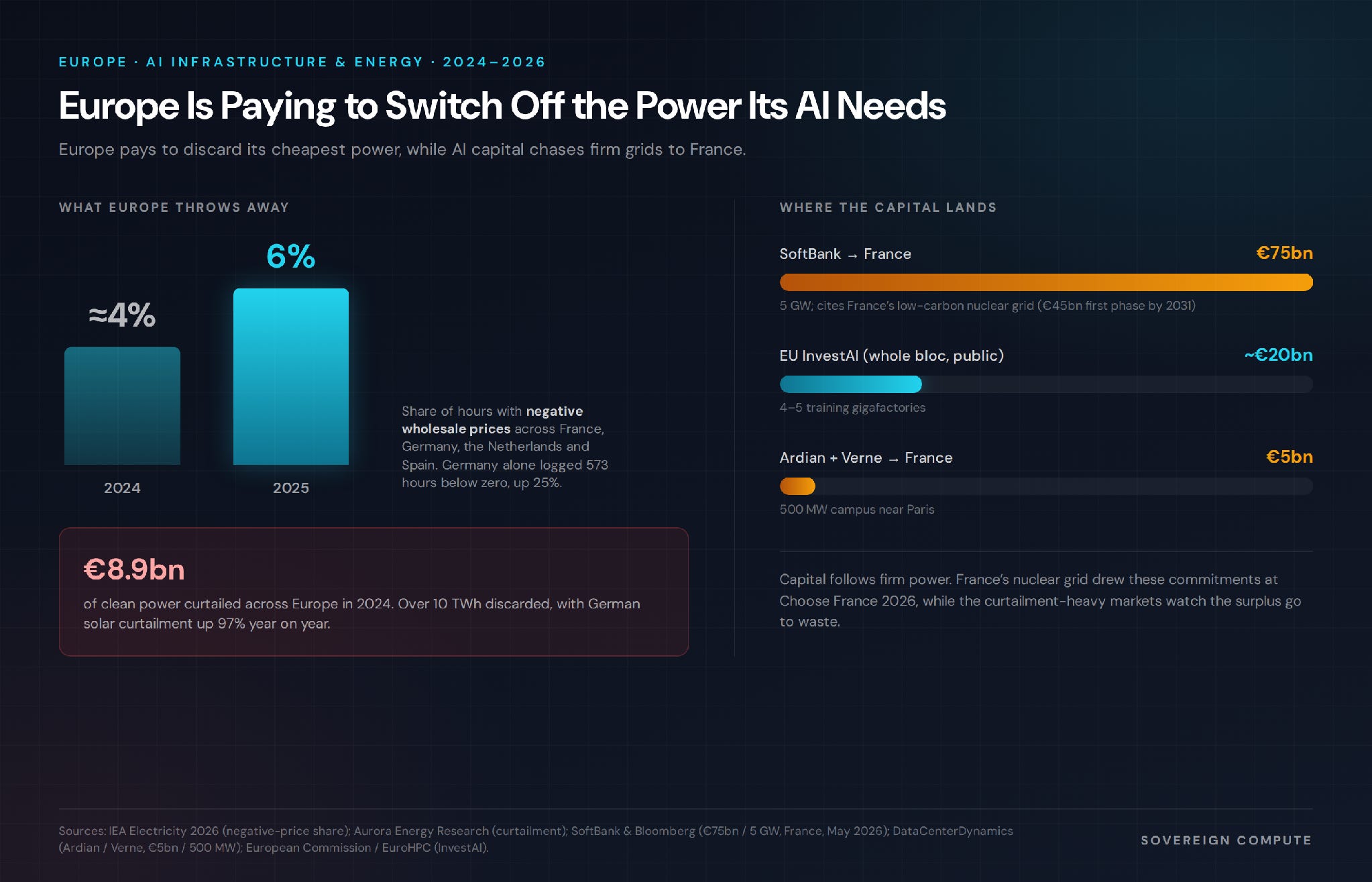

Europe pays to discard its cheapest power, then builds an AI strategy around the energy it says it lacks.

In 2025, wholesale electricity prices in France, Germany, the Netherlands and Spain dropped below zero in about one hour out of every sixteen, up from one in twenty-five a year earlier, according to the IEA. Germany alone recorded 573 hours of negative prices, a 25% rise. A negative price means there is more electricity on the market than the system can use, so producers that keep generating are effectively paying to offload their power rather than being paid for it. As this publishes, a June heatwave has pushed solar output high enough to send prices below zero again across parts of the continent.

Throwing that power away carries a significant bill. Aurora Energy Research puts the cost of curtailing renewables across Europe at €8.9 billion in 2024, with more than 10 terawatt-hours of clean generation discarded and German solar curtailment up 97% in a single year. Britain spent £1.47 billion paying wind farms to stop and gas plants to start. This is the cheapest electricity Europe produces, and the continent pays twice: once to build the turbines, again to switch them off.

The waste lowers no one’s bill because the power is stranded. Cheap renewable supply sits in the wrong place at the wrong moment, behind a grid that cannot move it. Average EU wholesale power ran near twice US levels in 2025 even with the surplus. The European Commission now estimates €1.2 trillion in grid investment is needed by 2040, up from a €584 billion figure for 2030. By one survey of sixteen countries, around 1,700 GW of renewable projects wait in connection queues, more than three times what the EU’s 2030 targets require, and cross-border lines average 5.6 years to permit. In the Netherlands, roughly 12,000 companies sit in line for a connection.

The capital is arriving, and where it lands settles the argument. At the Choose France summit in late May, SoftBank committed up to €75 billion to develop 5 GW of AI data center capacity in France, its largest AI infrastructure investment in Europe, with €45 billion and 3.1 GW in a first phase by 2031. Ardian and its platform Verne added up to €5 billion for a 500 MW campus near Paris. Both named the same draw: France’s low-carbon nuclear grid and the firm, steady power it supplies, with Schneider Electric among the industrial partners. The money goes where the power is firm and the connection clears.

That routing exposes a split inside Europe.

France can take gigawatts because nuclear baseload holds its prices steady and its grid clears. The curtailment sits in Germany, Spain, the Netherlands and the United Kingdom, where the surplus is wind and solar that the grid cannot move. Capital follows firm power to the market that already solved the question, while the markets richest in cheap clean electricity watch it pass. Brussels’ own InvestAI programme, about €20 billion for four or five training gigafactories, is a fraction of what a single foreign commitment now brings to France alone.

The assets Europe actually holds point in a different direction. ASML remains the only company on earth that builds the lithography machines advanced chips require, a chokepoint no rival can route around. Open-weight, data-resident models, Mistral among them, win regulated buyers like the French armed forces and HSBC, who pay for sovereignty even when a benchmark lags. And the stranded clean power is a siting advantage for compute that can run when the wind blows and pause when it drops. Batch inference and training checkpointing tolerate that rhythm; latency-critical work does not. The Gulf understood the principle early and priced energy as the foundation of its compute build. Europe sits on a comparable surplus, but it is not leveraging in the same way.

The opening is narrow and conditional. Flexible compute can monetise wasted power only where it co-locates behind the constraint, and only if connection and permitting reform arrives. That reform is the variable worth watching. For investors, the value accrues to whoever pairs interruptible compute with curtailment hotspots, to storage that captures the midday glut, and to the connection queue itself. Europe’s compute future runs through its grid, and the grid is the slowest thing it builds.

Sources

IEA Electricity 2026 (negative-price share, EU vs US wholesale): [link] Aurora Energy Research via Clean Energy Wire (€8.9bn curtailment, 2024): [link] Euronews (UK curtailment cost; heatwave negative prices): [link]

European Grids Package via GLOBSEC (€1.2tn by 2040): [link] European Commission / EuroHPC (InvestAI gigafactories): [link]

SoftBank (€75bn / 5 GW France commitment, May 2026): [link] DataCenterDynamics (Ardian / Verne €5bn / 500 MW): [link] Ember European Electricity Review 2026: [link]

A note on independence: All opinions shared in this newsletter are my own and do not reflect the views of dmg events, ADIPEC, or any affiliated organizations. This is personal analysis, not institutional positioning.