AI Is Racing to Replace Rare Earths. China Already Replaced US Chips.

The asymmetric decoupling is already visible in the data.

Beijing controls roughly 60% of global rare earth mining and around 85–90% of the refining capacity for the heavy rare earths used in permanent magnets, which are critical for physical AI (robotics). That position took three decades to build. The United States and its allies are now racing to dismantle it through AI-accelerated materials science, aiming to discover alternative materials that can replace rare-earth elements.

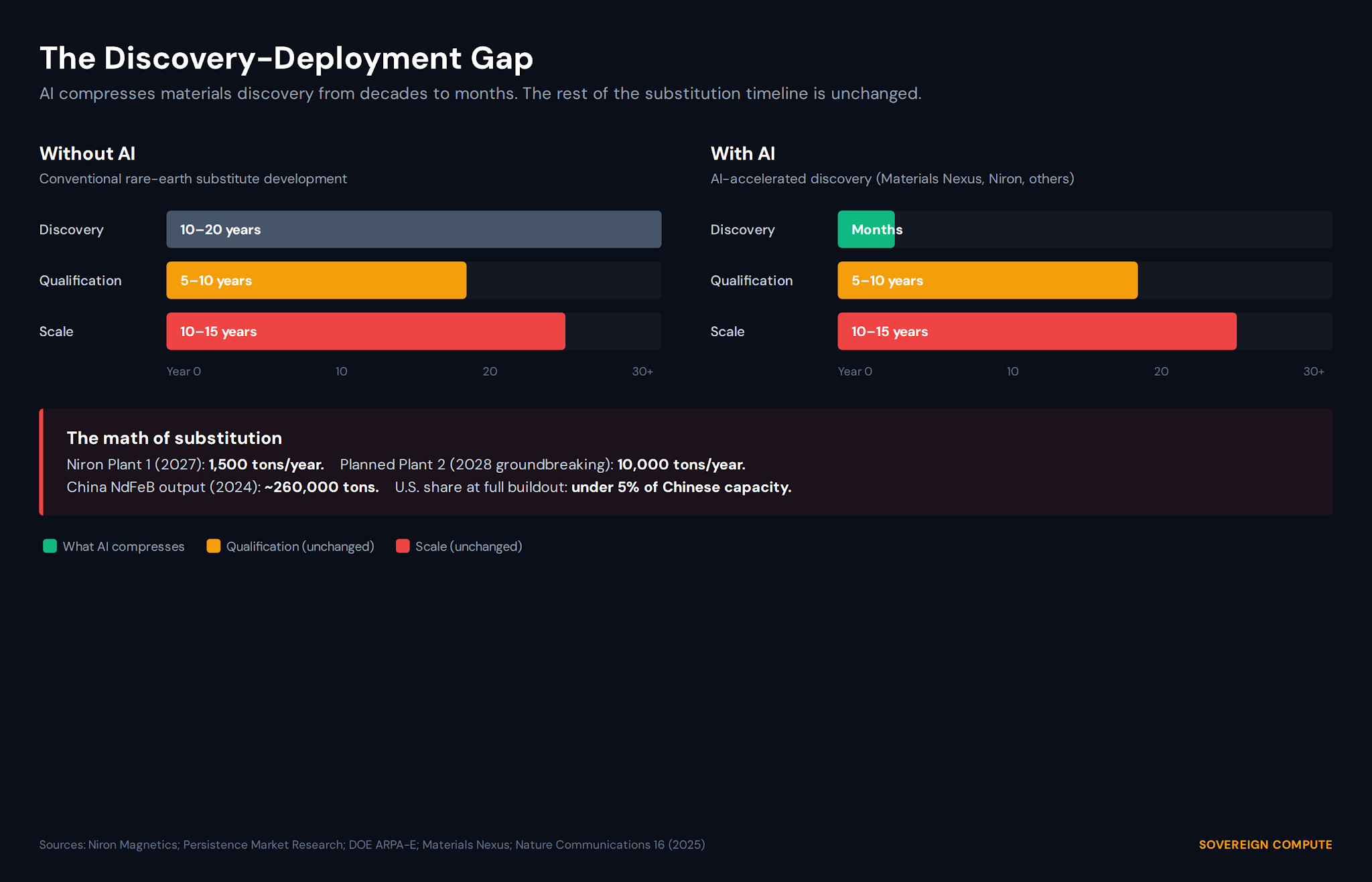

The evidence is there. Materials Nexus designed a rare-earth-free magnet on an AI platform in 2024 at roughly 200 times the pace of conventional methods. The University of New Hampshire built an AI database of 67,573 magnetic materials and identified 25 previously unrecognized compounds that hold their properties at elevated temperatures (Nature Communications, 2025). Niron Magnetics, with DOE backing going back to a $17.5M ARPA-E grant in 2022, broke ground in September 2025 on a 1,500 ton/year iron-nitride magnet plant in Minnesota, operational in early 2027, and in March 2026 announced a second, $1.8B, 10,000 ton/year facility.

That race is real. It is also slower than the alternative race China is winning.

AI compresses one stage of substitution and leaves the others untouched. Discovery moves from decades to months. Qualification cycles for permanent magnets in industrial motors, defense, and aerospace still run five to ten years due to safety-critical regulatory requirements in defense and aviation. Scale takes longer. Niron’s 1,500 ton/year Plant 1 in 2027, against Chinese NdFeB output of roughly 260,000 tons in 2024, is well under one percent of Chinese capacity. The planned second plant would bring the U.S. total to 11,500 tons by the end of the decade. Replacing the Chinese magnet supply chain is a fifteen-to-twenty-year program, even with AI on the discovery side. China built it in three decades. Unwinding it will take comparable time.

This timeline asymmetry is what the United States has been paying for since 2025. After Beijing imposed export controls on seven heavy rare earths in April 2025 (dysprosium and terbium prices roughly tripled in Western markets) and extended jurisdiction extraterritorially in October to any foreign product containing 0.1% Chinese rare earth content, Washington negotiated a truce at Busan on October 30, 2025. Per the White House Fact Sheet, China suspended the October 9 controls for one year and issued general licenses for rare earths, gallium, germanium, antimony, and graphite. In exchange, the United States cut fentanyl-related tariffs from 20% to 10%, paused a threatened 100% additional tariff, suspended a sanctions-affiliate rule for a year, and extended certain Section 301 exclusions. The deal expires around October 2026.

The H200 chips were supposed to be Washington’s other card. Trump authorized H200 sales to China on December 8, 2025, with a 25% revenue share to the U.S. Treasury, and licenses were issued in January 2026 to around ten Chinese firms. As of mid-May 2026, no H200 has shipped. Beijing has declined to approve purchases, and the Trump-Xi Beijing summit in May ended with no movement on chip exports. The reason sits on the demand side. DeepSeek released V4 on April 24, 2026, with day-zero inference support on Huawei’s Ascend 950PR platform, having granted Huawei pre-release kernel access. Alibaba’s T-Head GPUs reached scaled mass production. ByteDance lifted 2026 AI capex to roughly $30B with a rising share going to domestic chipmakers. Nvidia’s footprint in China’s frontier AI datacenter deployments has fallen to effectively zero from approximately 95% before export controls tightened. The H200 ultimately carried far less strategic leverage than Washington assumed.

The early evidence is of two parallel sovereign stacks forming at different speeds. The United States is using AI to substitute the material layer, with first commercial capacity in 2027 and meaningful scale in the 2030s. China is using policy and capital to substitute the chip layer, with frontier models already running in production on domestic chips in 2026. Neither has solved the problem, but both have demonstrated the problem is solvable on a sub-fifteen-year timeline.

For investors and sovereign AI buyers, the read is precise. The transition window is roughly the next decade. During it, U.S. policy is constrained by rare earth dependency, and Chinese policy is constrained by chip dependency only at the leading edge. The trade Washington offered was a card Beijing chose not to play, because the cost of waiting was lower than the cost of accepting U.S. routing through a 25% surcharge. The currency of decoupling is shifting from chips to materials. The side that closes its gap first sets the terms of the next decade.

Sources

• IEA, Rare Earth Elements analysis and critical minerals commentary (2025–2026)

• White House Fact Sheet on the Trump-Xi trade deal (November 1, 2025)

• China Briefing, Trump-Xi Meeting Outcomes and Implications (November 2025)

• CSIS, China’s New Rare Earth and Magnet Restrictions Threaten U.S. Defense Supply Chains (October 2025)

• CNBC, U.S. clears H200 chip sales to 10 China firms (May 14, 2026)

• Artificial Intelligence News, The Nvidia H200 China deal survived the Trump-Xi summit (May 2026)

• Nvidia Form 10-Q, Q1 FY2026

• Itani, Zhang, Zang, The northeast materials database for magnetic materials, Nature Communications 16 (2025), DOI: 10.1038/s41467-025-64458-z

• Beeson et al., C16 Phase High Entropy Borides, Advanced Materials (2025), DOI: 10.1002/adma.202516135

• Materials Nexus rare-earth-free magnet announcement (June 2024)

• Niron Magnetics Plant 1 groundbreaking (September 2025); Wood EPCM contract (January 2026); $1.8B second plant site selection (March 2026)

• Persistence Market Research and IDTechEx on permanent magnet market sizing (2025)

• Strategic Metals Invest retail benchmark prices, dysprosium and terbium (May 19–20, 2026)

• ChinaTalk, DeepSeek V4 (April 2026); Reuters on Huawei Ascend day-zero V4 support (April 24, 2026)

Sovereign Compute is an independent publication. Views expressed are those of the author and do not represent the views of any affiliated organization.