A Full-Stack Framework for AI Infrastructure Investing

The tables below identify companies and assets that illustrate the thesis across different structural forces.

What this is — and what it isn’t

This is a one-off analytical piece. It is not a recurring newsletter, not an investment advisory service, and not a solicitation. It presents a structural framework for understanding the AI infrastructure buildout and maps that framework to the sectors and asset classes where it is most directly expressed.

The tables below identify companies and assets that illustrate the thesis across different structural forces. They are not a portfolio, not a set of recommendations, and carry no suggested allocations or weightings. They are reference points for further research that you, the reader, can conduct — a starting map, not a set of directions.

The goal is to give you a way of thinking about AI infrastructure investing that you can apply on your own terms, with your own research, and in consultation with a licensed financial adviser.

The thesis: Five structural forces — energy demand, sovereign AI buildout, chip supply chain geopolitics, decentralised compute, and strategic mineral bottlenecks — are converging to reshape global capital flows. The companies and assets that sit at the intersection of these forces may define the next decade of returns.

1. The Macro Brief: The $650 Billion Collision

We are living through the largest infrastructure buildout in human history, and most investors are watching it through the wrong lens.

In February 2026, the four largest technology companies on earth collectively committed to spending approximately $625 billion in capital expenditures this year alone. Amazon will deploy $200 billion, Alphabet $185 billion, Meta $135 billion, and Microsoft $105 billion. These are not projections or aspirations. They are board-approved budgets already flowing into concrete, copper, and silicon.

This spending is colliding with a physical world that cannot absorb it. The US grid interconnection queue contains 2,600 GW of projects with a median wait of five years. The European Union has 1,700 GW stuck in similar delays. Seventy percent of American transmission lines are more than 25 years old. The April 2025 Iberian Peninsula blackout demonstrated what happens when aging grids meet exponential demand.

On February 25, NVIDIA reported its fiscal Q4 2026 results: $68.1 billion in revenue, up 73% year-over-year, with data center revenue hitting $62.3 billion. The company guided Q1 to $78 billion, beating estimates by $5.4 billion. The stock dropped 5.5% the following day, erasing $260 billion in market capitalisation. The market has shifted from asking whether AI infrastructure spending is real to asking whether the returns on that spending will materialise.

This is the central tension of 2026, and it creates the analytical framework this piece is built around.

The Five Forces in March 2026

Energy-AI Convergence. The IEA projects global data centre electricity consumption will double to 945 TWh by 2030, growing four times faster than total electricity demand. In the US alone, data centre power demand is projected to reach 134 GW by 2030, nearly tripling from today. This is not incremental growth; it is a step-change in how electricity is allocated globally.

Sovereign AI Infrastructure. Nations are treating compute capacity as a strategic asset. The UAE’s MGX fund targets $100 billion in AI and semiconductor investments. The G42/OpenAI/NVIDIA Stargate campus aims for 5 GW of capacity. Saudi Arabia’s HUMAIN subsidiary has secured $20 billion in partnerships targeting 6.6 GW by 2034. These are not venture bets; they are sovereign industrial policy backed by trillions in wealth fund capital.

Chip Supply Chain Geopolitics. The AI OVERWATCH Act advanced through committee in January 2026, proposing a statutory two-year ban on Blackwell-class chip exports to China. This is a material escalation from administrative BIS controls. Meanwhile, the hyperscaler shift toward custom ASICs is fragmenting what was a near-monopoly: the AMD-Meta five-year deal, valued at $60–$100 billion, signals the beginning of the inference era where custom silicon competes with merchant GPUs.

Decentralised Compute. Decentralised GPU networks are generating real revenue. The DePIN sector produced approximately $150 million in on-chain revenue in January 2026. Render Network has expanded beyond rendering into AI inference through its Dispersed subnet. Akash Network’s Burn-Mint Equilibrium code reached completion in February 2026 with mainnet launch scheduled for March 30. These are no longer speculative protocols; they are nascent utility markets. But they remain small relative to hyperscaler revenues, and intellectual honesty demands we acknowledge that.

Strategic Minerals. The top three refining nations control 86% of key energy minerals. China holds 80%+ of global graphite and rare earth processing. The IEA projects copper and lithium deficits of 30–40% by 2035. Every GPU, every data centre, every grid upgrade depends on physical materials whose supply chains are geographically concentrated and politically vulnerable.

What the Market Is Missing

Most AI investment analysis focuses on software companies and chip designers. The real bottleneck — and therefore the real analytical gap — is in the physical infrastructure layer: the power companies signing data centre contracts, the nuclear operators restarting reactors, the copper miners struggling to meet demand, the networking companies building the backend fabric that connects millions of GPUs.

This piece maps the full stack. From uranium in the ground to tokens on-chain.

2. Thesis Deep Dive: The Inference Rotation

Why the AI Hardware Winners of 2025 May Not Be the Winners of 2027

The DeepSeek R1 release in early 2025 proved that frontier-level AI performance could be achieved at one-tenth the compute cost of comparable models. This single development reshaped the investment landscape for AI infrastructure in ways the market has not yet fully absorbed.

The immediate reaction was a $593 billion wipeout in NVIDIA’s market capitalisation. But the structural implication runs deeper than one company’s stock price. DeepSeek demonstrated that the AI compute market is bifurcating: training workloads remain concentrated among a handful of frontier labs willing to spend billions on GPU clusters, while inference workloads — running models in production for billions of users — are shifting toward efficiency, custom silicon, and cost optimisation.

This is not a bearish development for AI infrastructure spending. The Jevons Paradox applies: when compute becomes cheaper per unit, total demand expands because more applications become economically viable. But it does change who captures value.

The Training-to-Inference Shift

NVIDIA built its dominance on training. Its CUDA software ecosystem and GPU architectures are purpose-built for the massively parallel matrix operations that training requires. For training, NVIDIA remains unchallenged. No serious competitor has emerged for frontier model training at scale.

Inference is different. Running a trained model in production requires different optimisations: lower latency, higher throughput per watt, lower cost per token. These requirements favour custom Application-Specific Integrated Circuits designed for specific workloads rather than general-purpose GPUs designed for everything.

This is where Broadcom has quietly become the most important company in AI that most investors have never heard of. Broadcom designs the custom ASICs that hyperscalers use for inference: Google’s Tensor Processing Units, Meta’s custom accelerators, and most recently OpenAI’s “Titan” chips under a partnership estimated at $100–200 billion over multiple years. Broadcom’s AI revenue is projected to hit $40 billion in fiscal 2026, with a $73 billion hardware backlog providing multi-year visibility. The February 2026 AMD-Meta five-year deal, valued at $60–100 billion, further confirms that hyperscalers are diversifying away from NVIDIA’s merchant GPU model.

The inference shift also creates opportunity in the decentralised compute layer. Networks like Render and Akash are fundamentally inference platforms. They cannot compete with NVIDIA’s DGX clusters for frontier training. But for running models in production at low cost, with geographic distribution and without hyperscaler lock-in, they offer a structural alternative that becomes more compelling as inference demand explodes.

The Analytical Implication

The inference rotation is not a threat to AI infrastructure spending. It is a redistribution of who captures value within that spending. Understanding this redistribution — and identifying which companies and assets are positioned for it — requires mapping the full stack: from the chip designers and contract manufacturers building the custom silicon, to the power companies and data centre operators housing it, to the decentralised networks offering an alternative distribution layer.

3. The Full-Stack Framework: Mapping Forces to Sectors

The core design principle behind this framework is that an investment thesis should be directly expressed through the assets it identifies. When you read about grid constraints, the relevant sector is power generation. When you read about export controls, the relevant sector is semiconductor fabrication. When you read about mineral bottlenecks, the relevant sector is upstream mining. When the thesis and the research point in the same direction, the analytical alignment is strong.

The tables below organise the five structural forces into three categories — infrastructure backbone, thematic plays, and digital asset infrastructure — and identify the companies and assets most directly connected to each force. These are analytical reference points for further research, not recommendations or a portfolio. No weightings or allocations are implied. Readers should conduct their own due diligence and consult a licensed financial adviser.

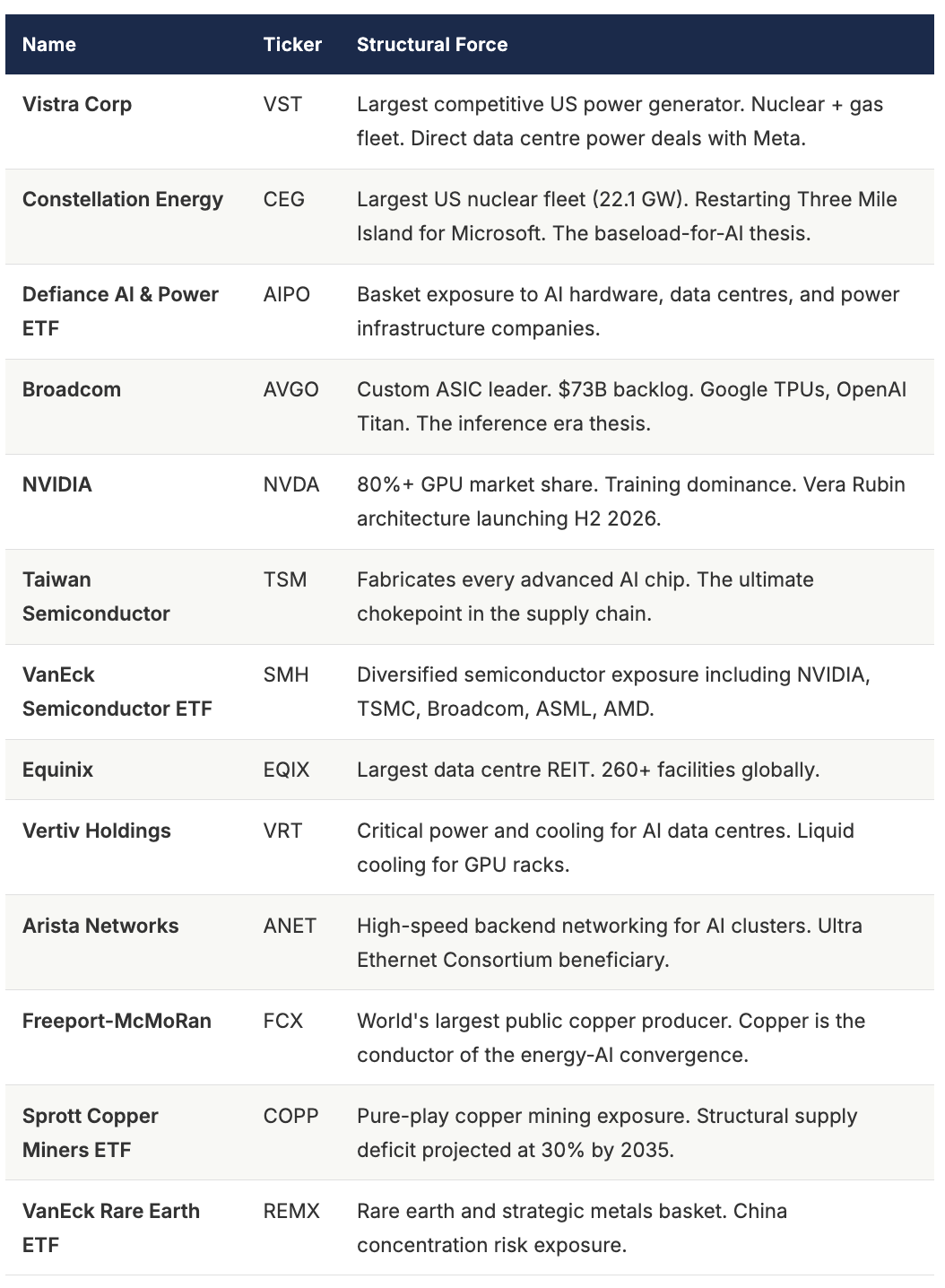

Category 1: Infrastructure Backbone

These names directly capture the physical forces the thesis describes. They rise and fall based on actual infrastructure buildout, not sentiment. This is where thesis-to-sector alignment is strongest.

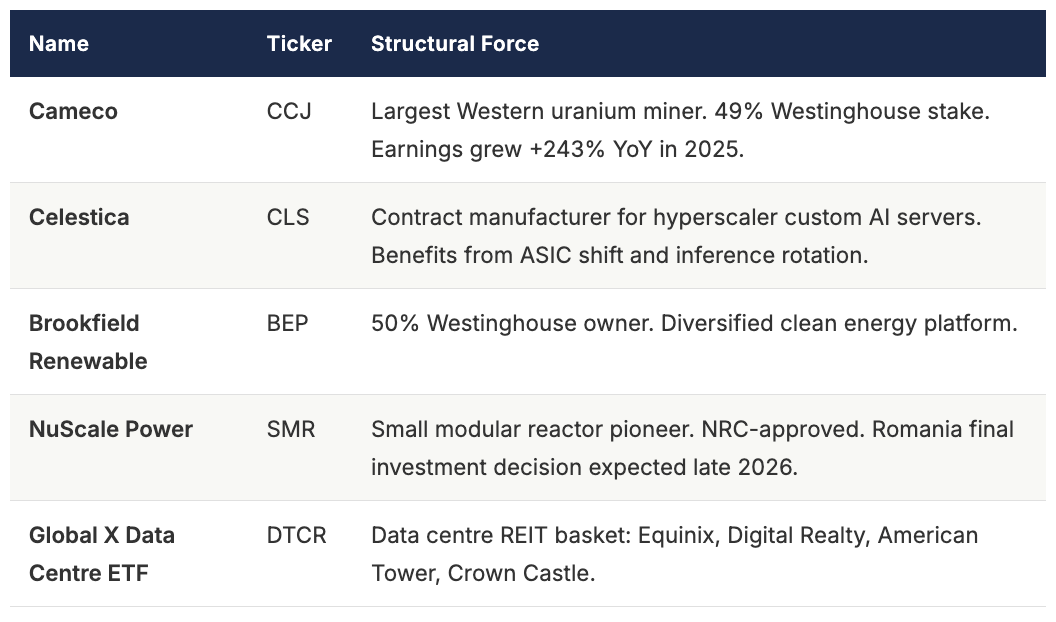

Category 2: Thematic Plays

These names connect to themes where domain-specific intelligence — from energy conferences, sovereign wealth fund activity, and ASEAN energy policy — provides analytical context that generic equity research may not capture.

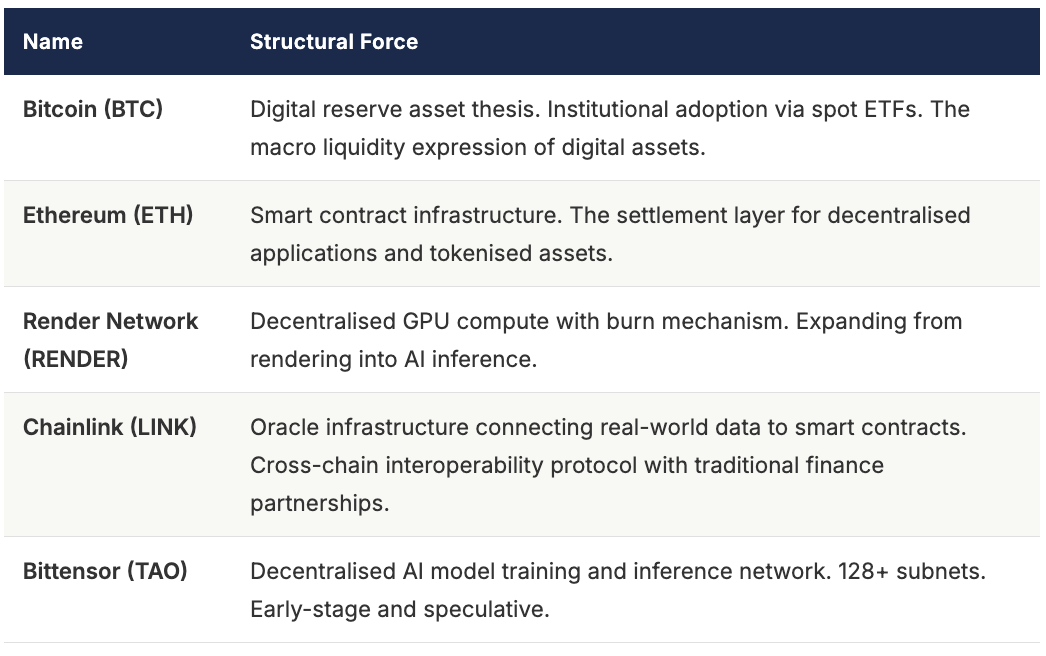

Category 3: Digital Asset Infrastructure

The Sovereign Compute thesis extends to the decentralised compute and on-chain infrastructure layer. These assets represent the digital side of the same structural forces — distributed GPU compute, cross-chain settlement infrastructure, and decentralised AI model training. Digital assets are highly volatile, speculative, and may result in total loss of capital. The names below illustrate where the thesis intersects with the digital asset ecosystem; they are not recommendations to purchase or hold any asset.

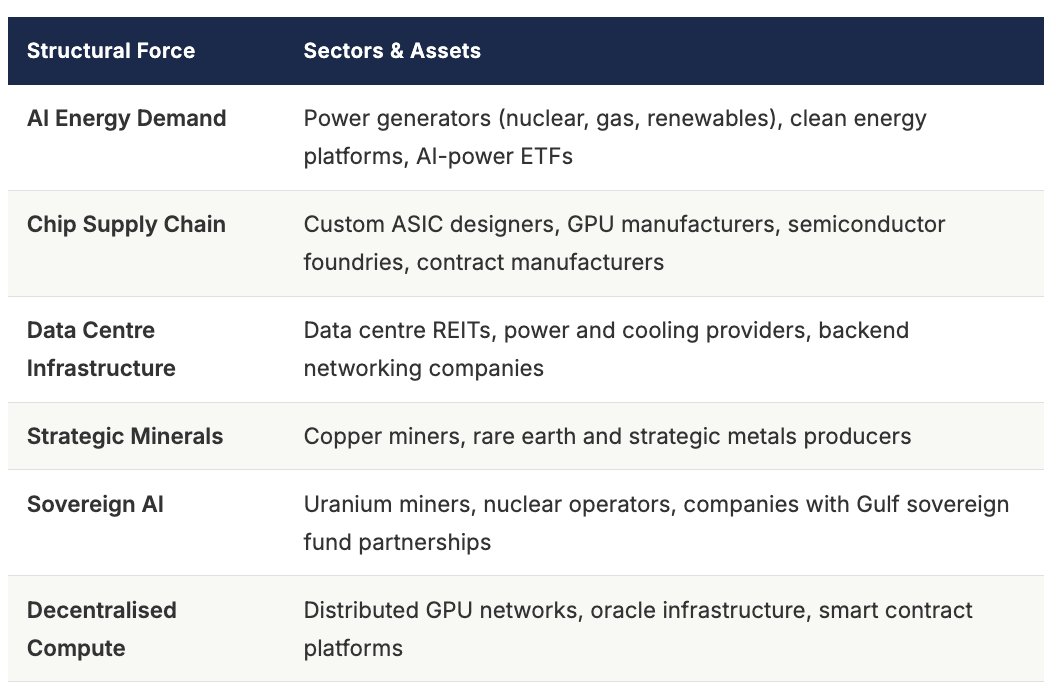

Force-to-Sector Alignment

The table below maps each structural force to the sectors and asset categories where it is most directly expressed. This is the core of the analytical framework — the idea that the investment thesis and the assets you research should point in the same direction.

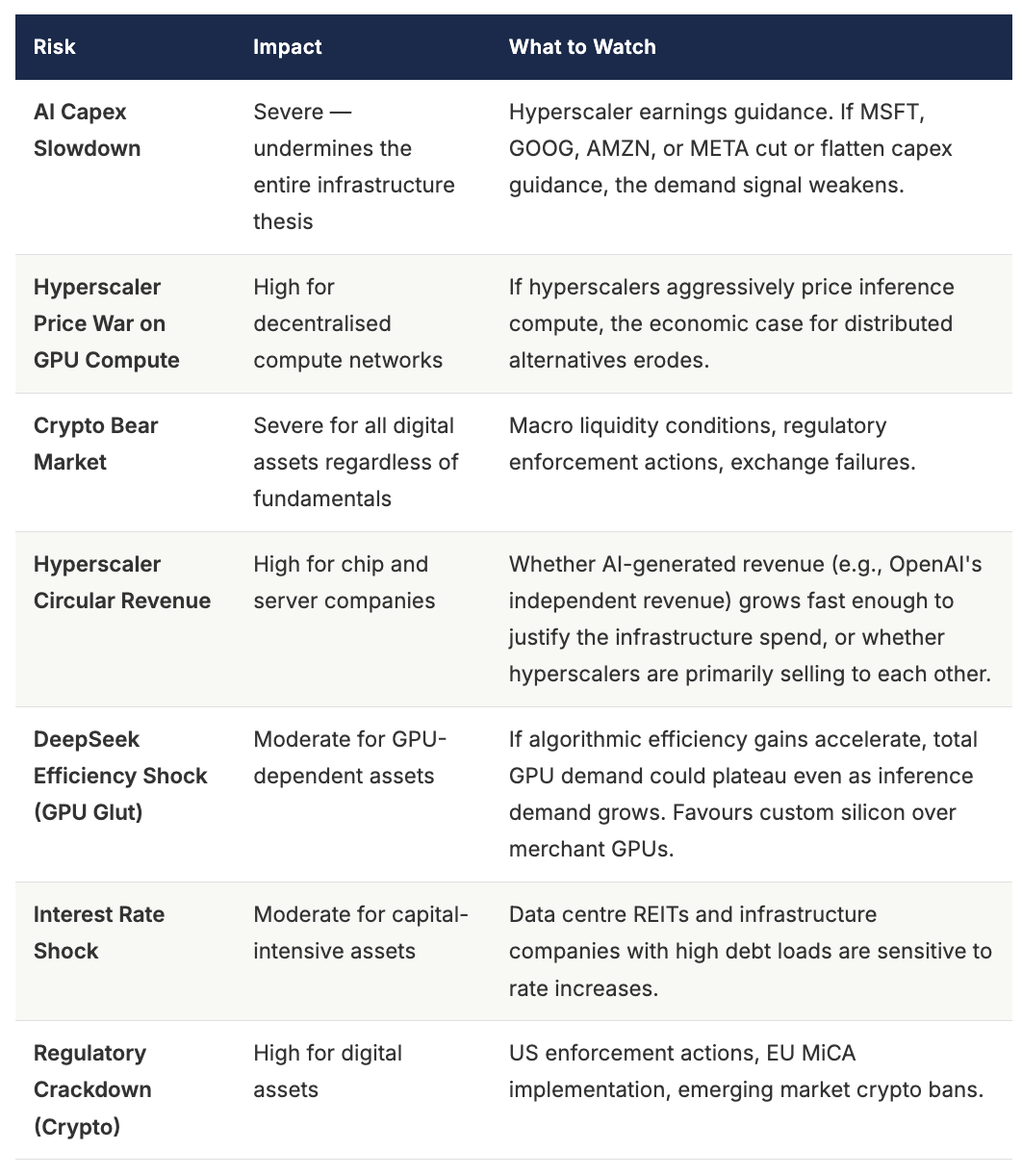

4. Risk Framework

Intellectual honesty demands that any analytical framework acknowledge what could make it wrong. The following risks could undermine or invalidate the thesis above.

The bear case is real. If AI capex slows materially and crypto enters a prolonged downturn simultaneously, assets connected to this thesis would face significant drawdowns. The infrastructure-heavy sectors (power, semis, data centres) would fare better than digital assets in that scenario, but neither would be immune. Any framework that tells you only the bull case is not worth your time.

5. Catalyst Calendar

The following events represent known structural catalysts that could materially affect the thesis over the coming months.

6. How to Apply This Framework

This piece gives you a lens. What you do with it is up to you.

The five structural forces — energy demand, chip supply chains, data centre infrastructure, strategic minerals, and sovereign AI buildout — are the analytical backbone. When you read news about any of these forces, ask: which sectors and assets are most directly connected? The force-to-sector alignment table above is your map.

If the thesis resonates, your next steps are your own research. Examine the companies and assets named above. Read their earnings transcripts. Assess whether the structural force behind each name is strengthening or weakening. Decide which sectors match your own risk tolerance, time horizon, and financial situation. Consult a licensed financial adviser before making any investment decisions.

The framework is the contribution. The decisions are yours.

Disclaimer & Disclosures

This is a one-off analytical piece published for general educational and informational purposes only. It is not a recurring advisory service, not a managed portfolio, and not a solicitation to buy, sell, or hold any asset. Nothing in this publication constitutes personalised investment advice, financial advice, virtual asset advisory services, or a personal recommendation to any reader.

The companies, ETFs, and digital assets named in the tables above are identified as analytical reference points to illustrate the structural thesis. They are not recommendations. No allocations, weightings, or position sizes are suggested or implied. Readers are solely responsible for their own investment decisions and should conduct independent research and consult a licensed financial adviser before making any investment.

Cryptocurrency and digital asset investments are highly volatile and speculative. The value of such investments may decline significantly and may result in total loss of capital. Past performance of any asset discussed does not guarantee, predict, or indicate future results.

This piece is published by Ivan Ferrari in a personal capacity. Ivan Ferrari is VP of ADIPEC & Business Development at dmg events. This publication operates independently of dmg events and does not represent the views or analysis of dmg events or any affiliated entity. Ivan Ferrari may hold personal positions in assets discussed in this piece.

This publication is not regulated by VARA, the SCA, or any financial regulatory authority. It does not provide suitability assessments, maintain client agreements, or offer tailored recommendations to any reader.

SOVEREIGN COMPUTE

sovereigncompute.substack.com

© 2026 Ivan Ferrari. All rights reserved.